I Will Teach You To Be Rich Summary and Key Lessons

I Will Teach You to Be Rich by Ramit Sethi is a practical personal finance book built around one central idea: money should support the life you actually want. Sethi rejects shame-based advice, extreme frugality, and endless financial overthinking. Instead, he teaches readers to build simple systems for credit, banking, saving, investing, debt repayment, and major life decisions.

The book is direct, opinionated, and action-focused, but it also makes room for personal choice. Its goal is not just to help readers become richer on paper, but to help them design a “Rich Life” that feels meaningful, flexible, and sustainable.

Summary

Foundational Principles

At the outset, Sethi introduces readers to the core philosophy behind his approach: The concept of a “Rich Life.”

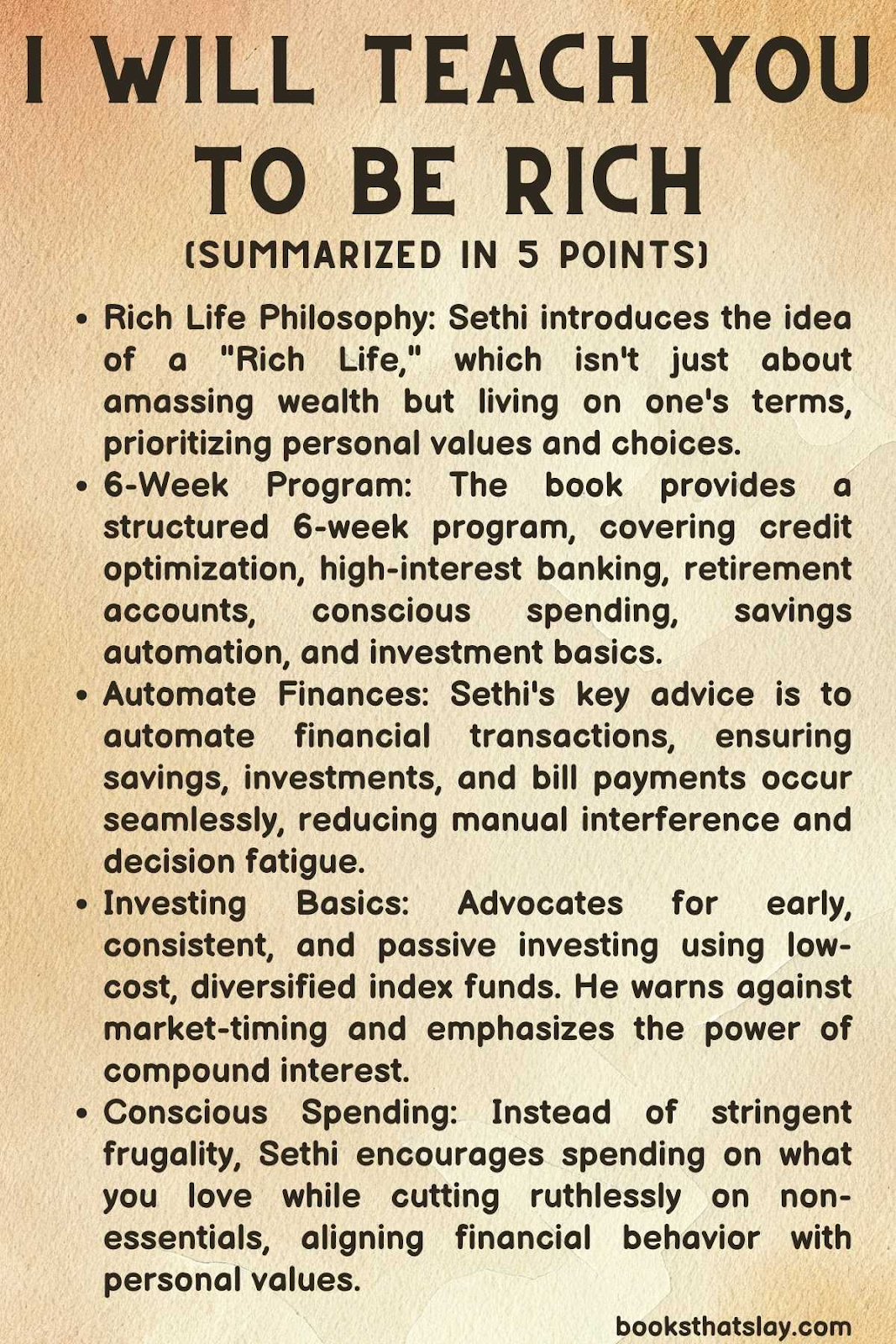

A Rich Life is subjective and varies for each person; it’s not just about having vast sums of money but about using money as a tool to lead a life filled with choices and lived on one’s own terms.

He emphasizes the importance of understanding and challenging our own beliefs about money, derived from our upbringing and societal pressures. Sethi critiques the standard advice of cutting back on small daily expenses like lattes and instead focuses on big wins, such as negotiating for a higher salary or optimizing large monthly expenses.

The 6-Week Program

Sethi introduces a 6-week program to achieve financial wellness. Each week is dedicated to a specific aspect of personal finance.

In the first week, he talks about setting up credit cards, learning about credit scores, and how to optimize for rewards. The second week is about setting up no-fee, high-interest bank accounts.

By the third week, you are introduced to opening a Roth IRA and 401(k). In the fourth week, he explains how to figure out how much you’re spending and introduces the concept of “conscious spending.”

The fifth week covers automated savings. The final week is about investing and learning the difference between stocks, bonds, and other investment vehicles.

Automating Finances

A cornerstone of Sethi’s philosophy is the idea of “setting and forgetting” your finances. Instead of constantly worrying about every penny, Sethi advises automating finances so that money flows where it needs to without regular intervention.

This includes automatic transfers to savings accounts, investments, and bills. By automating, one ensures that they’re saving and investing consistently without the pain of decision-making every time. It’s a behavioral trick that harnesses the power of inertia for financial gain.

Investing and Growth

Sethi demystifies the world of investing, stressing the importance of starting early due to the magic of compound interest.

He warns against trying to time the market or falling for the allure of “hot stocks.” Instead, he champions a long-term, passive investment strategy using low-cost, diversified index funds. He breaks down the nuances of asset allocation and underscores the significance of continued investments, especially during market downturns.

He also touches on the importance of negotiating salaries and raises, given that one’s earning potential is the biggest tool in the arsenal for amassing wealth.

Conscious Spending and Living Richly

Sethi’s approach to spending is refreshingly unconventional.

Rather than advocating for relentless frugality, he introduces the idea of “conscious spending” – spending exuberantly on the things you love while cutting costs mercilessly on things you don’t care about.

This is tied back to the concept of a “Rich Life,” which is personalized for every individual. Whether one’s passion is travel, dining out, or collecting rare items, Sethi’s philosophy permits and even encourages lavish spending, as long as it’s done consciously, joyfully, and without compromising long-term financial goals.

The Six-Week Program

Week 1: Optimize Your Credit Cards

Sethi aggressively defends credit cards, arguing that when used correctly, they are the best short-term financial tool available. They offer fraud protection, rewards, cash back, and most importantly, they help you build a credit history.

The Importance of Credit

Your credit score (FICO score) is the most critical number in your financial life. A high credit score will save you tens of thousands of dollars on the biggest purchases of your life, specifically your mortgage and auto loans, by securing you the lowest interest rates.

Actionable Steps for Week 1:

- Check your credit score: Know where you stand.

- Set up auto-pay: Never, ever miss a payment. A single late payment can crater your credit score and cost you severely in late fees and raised interest rates. Set your credit card to automatically pay the full balance from your checking account a few days before the due date.

- Negotiate away your fees: If you are paying an annual fee on a card that doesn’t provide outsized value, call the bank and ask them to waive it. If you have late fees, use Sethi’s script: “Hi, I saw a late fee on my account. I’ve been a good customer for X years, and I’d like to have it removed.” Banks will often waive it for good customers.

- Lower your interest rate (if you have debt): Call your credit card company and ask for a lower APR.

- Get more credit (to improve your score): Call your provider and ask for a “credit limit increase.” As long as you don’t increase your spending, this lowers your “credit utilization rate” (the percentage of available credit you use), which instantly boosts your credit score.

If you have credit card debt: Sethi acknowledges both the “Snowball” (paying off smallest balances first for psychological wins) and “Avalanche” (paying off highest interest rates first for mathematical efficiency). He prefers the math of the Avalanche but urges readers to pick whichever one they will actually stick to.

Week 2: Beat the Banks

Most traditional big banks (like Bank of America or Wells Fargo) prey on their customers with minimum balance requirements, maintenance fees, and overdraft charges. Furthermore, their savings accounts offer near-zero interest rates. Week 2 is about firing bad banks and setting up a foundation of good ones.

The Two Accounts You Need:

- A Fee-Free Checking Account: This is the Grand Central Station of your money. All your income flows into here, and all your automated transfers flow out of here. Sethi highly recommends Charles Schwab’s Investor Checking because it has no fees, no minimums, and reimburses all ATM fees worldwide.

- A High-Yield Savings Account (HYSA): This is the parking lot for your short-term-to-medium-term goals (emergency fund, wedding, vacation, down payment). Traditional banks offer ~0.01% interest. Online banks (like Ally, Marcus, or Capital One) offer much higher rates. Because online banks have no physical branches, they pass the savings onto you in the form of higher yields.

Actionable Steps for Week 2:

- Open a high-yield savings account: Do not close your old accounts yet, just get the new one open and funded with a small amount.

- Open a fee-free checking account.

- Opt out of overdraft protection: Overdraft protection is a scam that allows banks to charge you $35 every time you overdraw your account by $1. Decline it. If you don’t have the money, your card should simply be declined.

- Transfer your funds and close the bad accounts: Move your money to the new accounts. If your old bank tries to charge you a fee to close or transfer, push back.

Week 3: Get Ready to Invest

This is the most critical week for long-term wealth building. Sethi explains that rich people do not get rich by saving; they get rich by investing. Because of inflation, money left in a savings account actually loses purchasing power over time. Investing is how your money makes money through the power of compound interest.

The Ladder of Personal Finance

Sethi provides a strict order of operations for where your money should go. You do not move to the next step until you have maxed out the current one.

- Step 1: Your Employer’s 401(k) Match. If your company offers a 401(k) match (e.g., they match 100% of your contributions up to 5% of your salary), you must contribute exactly that amount. This is literal free money and represents a guaranteed 100% return on investment.

- Step 2: Pay off toxic debt. Pay off your high-interest credit card debt or personal loans. You cannot effectively invest if you are losing 20% a year to credit card interest.

- Step 3: Open and fund a Roth IRA. A Roth IRA is an individual retirement account with a massive tax advantage: you contribute after-tax money, meaning it grows tax-free, and you pay zero taxes when you withdraw it in retirement. You should aim to contribute the legal maximum to this account every year.

- Step 4: Max out your 401(k). If you have maxed out your Roth IRA and still have money to invest, go back to your 401(k) and contribute up to the legal annual maximum.

- Step 5: HSA or Taxable Brokerage Accounts. If you are still maxing out the above (which means you are saving tens of thousands of dollars a year), you can look into Health Savings Accounts (if eligible) or standard, non-tax-advantaged brokerage accounts to invest further.

Actionable Steps for Week 3:

- Log into your HR portal: Check your 401(k) matching rules and adjust your contribution to get the full match.

- Open a Roth IRA: Use a low-cost brokerage firm like Vanguard, Fidelity, or Charles Schwab.

- Set up automated transfers: Set up an automatic monthly transfer from your checking account to your Roth IRA.

(Note: Week 3 is just about opening the accounts and moving the money into them. Week 6 covers what to actually buy once the money is inside).

Week 4: Conscious Spending

Budgets don’t work. They are backward-looking and make you feel guilty about the past. Sethi replaces budgets with a Conscious Spending Plan. This is a forward-looking plan that dictates where your money goes before you even see it.

You break your take-home pay (after taxes) into four distinct buckets.

The Four Buckets:

- Fixed Costs (50-60% of take-home pay):These are the non-negotiables. Rent/mortgage, utilities, internet, phone bill, insurance, car payments, groceries, and debt minimums. If your fixed costs are higher than 60%, you are living too close to the edge. You either need to increase your income or make a drastic cut (like moving to a cheaper apartment).

- Investments (10% of take-home pay):This is the money flowing into your 401(k) and Roth IRA. This is for long-term wealth (retirement). 10% is good, 15% is great, 20%+ means you will be very wealthy.

- Savings Goals (5-10% of take-home pay):This money goes into your High-Yield Savings Account. It covers short-term and medium-term goals. You should use sub-savings accounts for specific goals: “Emergency Fund” (3-6 months of living expenses), “Mexico Vacation,” “Down Payment,” or “Car Repairs.”

- Guilt-Free Spending (20-35% of take-home pay):This is the magic of the system. Once your fixed costs are covered, your investments are growing, and your savings goals are funded, the rest is yours to spend on whatever you want with zero guilt. Whether you want to spend 25% of your income on designer shoes, expensive dinners, or a ridiculous gaming setup, you can do it happily because the responsible work is already done.

The A La Carte Method

If you need to cut costs to hit these percentages, use the à la carte method. Cancel all subscriptions (cable, gym, streaming). Then, consciously buy them back one by one only if you truly miss them.

Week 5: Save While Sleeping (Automation)

Willpower is a depreciating asset. If you have to actively decide to log in and transfer money to savings every month, you will eventually fail. Week 5 is about connecting all the accounts you opened in Weeks 1-3 and implementing the Conscious Spending Plan you built in Week 4 into an automated machine.

The Money Flow:

Here is how your money should flow automatically every month:

- Payday (e.g., the 1st of the month): Your paycheck hits your checking account. (Note: Your 401(k) contribution was already deducted automatically by your employer before you even saw the money).

- The 5th of the month: Automatic transfers trigger from your checking account.

- Transfer X amount to your HYSA for your Savings Goals.

- Transfer Y amount to your Roth IRA for your Investments.

- The 7th of the month: Automatic bill pay handles your Fixed Costs (rent, utilities, etc.).

- The 10th of the month: Your credit card is automatically paid in full from your checking account. (You put all your day-to-day fixed costs and guilt-free spending on this card to get the points).

What’s left in your checking account? Exactly the amount of money you have designated for cash/debit “Guilt-Free Spending” for the rest of the month.

You spend roughly one hour setting up these recurring transfers. Once it’s done, you literally manage your finances in less than 60 minutes a month.

Week 6: The Myth of Financial Expertise

Now that your money is automatically flowing into your investment accounts (401k and Roth IRA), what do you actually buy?

Sethi dismantles the financial industry. He explains that financial pundits on TV, active fund managers, and stock pickers cannot consistently beat the market over the long term. If you try to pick individual stocks, you are gambling. If you pay an active manager a 1% or 2% fee to manage your money, they will eat up tens of thousands of dollars of your returns over your lifetime, and they will likely underperform a basic index.

The Solution: Passive Investing

You should invest passively. This means buying the entire market instead of trying to find the needle in the haystack.

- Index Funds: These are low-cost funds that simply track an index, like the S&P 500 (the 500 largest US companies). By buying an S&P 500 index fund, you own a tiny piece of all 500 companies. The expense ratios (fees) are incredibly low (often 0.04% or less).

- Asset Allocation: This is the most critical concept in investing. Asset allocation is how you divide your money among different categories (stocks, bonds, cash). Stocks are high-risk/high-reward. Bonds are lower-risk/lower-reward. In your 20s and 30s, you should be heavily weighted in stocks (90%+) because you have decades to ride out market crashes. As you get closer to retirement, you transition to bonds to protect your capital.

- Target-Date Funds (The Ultimate “Set It and Forget It” Solution):If you don’t want to rebalance your own portfolio, Sethi highly recommends Target-Date Funds. You pick the year you plan to retire (e.g., Vanguard Target Retirement 2060 Fund) and put 100% of your investment money into it. The fund automatically diversifies your money globally. More importantly, it automatically adjusts your asset allocation over time. In 2026, it is highly aggressive (mostly stocks). By 2055, it will automatically shift to a conservative portfolio (heavy in bonds). It is the perfect 85% solution for hands-off investors.

Actionable Steps for Week 6:

- Log into your 401(k) and Roth IRA.

- Select your investments: Look for low-cost, passive Index Funds or a single Target-Date Fund.

- Verify expense ratios: Ensure the fees on the funds you are buying are below 0.5% (ideally below 0.2%).

After Six Weeks

Once your automated money machine is built, you graduate to managing the “Big Wins” and navigating the psychological complexities of money in the real world.

Relationships and Money

Money is the number one cause of stress in relationships. Sethi advises discussing money early and often.

- The Pre-Nuptial Agreement: He advocates for pre-nups, framing them not as an expectation of divorce, but as a mutual agreement made with a clear head to protect both partners and force a transparent conversation about financial philosophies.

- Combining Finances: There is no one-size-fits-all approach. You can keep accounts completely separate, merge them completely, or use a “yours, mine, and ours” approach (a joint account for fixed costs and shared goals, and individual accounts for personal guilt-free spending). The key is communication and agreeing on a system.

- Paying for a Wedding: Weddings are notoriously expensive. Use the Conscious Spending philosophy here. Decide on the 1 or 2 things that matter most to you (e.g., the food and the photographer) and spend lavishly there, while ruthlessly cutting back on things you don’t care about (e.g., custom napkins or elaborate floral centerpieces).

Buying a Car

A car is not an investment; it is a rapidly depreciating liability.

- Buy Reliable: Buy a car known for longevity (like a Honda or Toyota).

- Hold for 10 Years: The true value of a car is realized if you drive it into the ground. Buy it, pay it off in 4-5 years, and then enjoy 5+ years of zero car payments.

- Negotiating: Use the internet to your advantage. Email multiple dealerships with the exact make, model, and trim you want, and ask them to give you their “out the door” price. Pit them against each other via email before you ever step foot on a lot.

The Truth About Real Estate: Renting vs. Buying

This is one of Sethi’s most controversial and heavily emphasized points. Society pushes the narrative that “renting is throwing money away” and buying a home is always the best financial decision. Sethi argues this is mathematically false in many high-cost-of-living areas.

- Phantom Costs of Homeownership: When you rent, your rent is the maximum you will pay that month. When you buy, your mortgage is the minimum you will pay. Homeowners must account for property taxes, maintenance (rule of thumb: 1-2% of the home’s value per year), insurance, closing costs, and opportunity cost (the down payment tied up in the house is not earning 8% in the stock market).

- When to Buy: You should only buy a house if:

- You plan to live in it for at least 10 years.

- You have a 20% down payment (to avoid Private Mortgage Insurance).

- Your total housing costs (mortgage + taxes + insurance + maintenance) do not exceed 28% of your gross income.

- You want to be a homeowner and deal with the maintenance.

- If you rent, take the money you save on phantom costs and invest it aggressively in the market. You can become extremely wealthy as a lifelong renter.

Salary Negotiation

This is the single biggest “Big Win.” Negotiating a $5,000 raise in your 20s, when factored into future raises and compound interest, can be worth hundreds of thousands of dollars over your career.

- Do your research: Know your market value using sites like Glassdoor or Payscale.

- Build a portfolio of accomplishments: Do not ask for a raise because you “need” it for a house or because of inflation. Ask for a raise because you have demonstrably added value to the company.

- The “Briefcase Technique”: When you sit down for the negotiation, pull out a multi-page document outlining exactly how you plan to solve the company’s biggest problems over the next 6-12 months. This shifts the dynamic from you begging for money to you proving you are an indispensable investment.

Before You Leave, Remember –

Your financial life is not static. Your income will change, your goals will shift, and your definition of a Rich Life will evolve.

- Annual Maintenance: Once a year, sit down and review your system. Check your asset allocation and rebalance it if necessary (unless you have a Target-Date fund, which does it for you). Review your insurance policies. Call your cable/internet providers and negotiate your rates.

- Celebrate Your Success: If you stick to the system, you will eventually find yourself with more money than you expected. Do not succumb to lifestyle creep (inflating your fixed costs as your income rises), but do allow your Guilt-Free Spending bucket to grow. If you’ve automated your savings and investments, spend the rest joyfully.

I Will Teach You to be Rich operates on a simple premise: stop trying to be an expert in the minutiae of finance, build a system that works automatically, focus your energy on earning more, and unapologetically spend money on the things that bring you immense joy.