23 Things They Don’t Tell You About Capitalism Summary and Analysis

23 Things They Don’t Tell You About Capitalism by Ha-Joon Chang is a clear, argument-driven guide to how modern capitalism actually works—and how the popular story about “free markets” often leaves out the messy parts. Written in the shadow of the 2007–2008 financial crisis, the book takes aim at common claims that markets are naturally fair, governments are always incompetent, and globalization automatically benefits everyone.

Chang uses short, focused essays to question these beliefs with history, examples from different countries, and plain reasoning. The result is an invitation to think like an informed citizen: to ask who benefits from certain rules, what trade-offs exist, and what a more stable and broadly shared prosperity might require.

Summary

In 23 Things They Don’t Tell You About Capitalism, Ha-Joon Chang responds to the global financial crisis by challenging the free-market mindset that became influential from the 1980s onward. He argues that many policy choices sold as “common sense” economics are really political decisions presented as neutral facts.

Instead of treating markets as forces of nature, he asks readers to notice the rules behind them, the power relationships those rules create, and the historical evidence that today’s rich economies used a variety of tools—often the very tools they now discourage poorer countries from using.

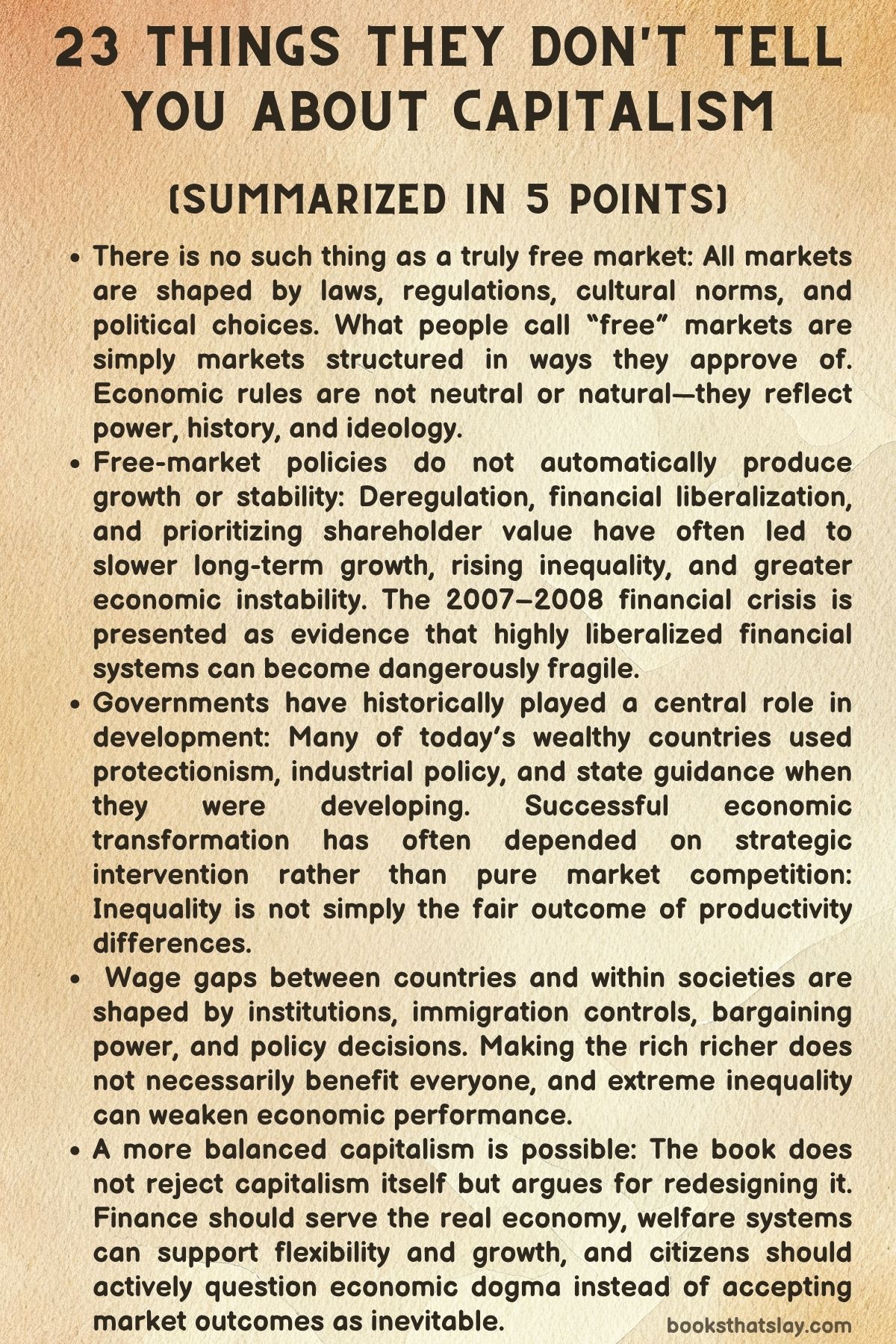

Chang begins with a basic claim: there is no such thing as a truly free market. Every market depends on laws and social norms that define what can be traded, who is allowed to participate, and how agreements are enforced.

Even widely accepted protections, like bans on child labor, were once attacked as unacceptable government interference. Over time, societies changed their minds about what should be legal and what should be restricted.

For Chang, that history shows that “freedom” in the market is not an objective condition that economists can measure like temperature. It is a label applied from a particular viewpoint.

One person’s “unnecessary regulation” is another person’s protection of public interests, and arguments about freedom often mask disagreements about values and priorities.

From there, Chang turns to how companies are governed. He argues that the popular idea that firms should be run mainly for shareholders produces harmful incentives.

Because most shareholders can buy and sell shares quickly, they often reward strategies that raise profits in the near term, even when those strategies weaken the company’s long-term capacity. He points to the rise of “shareholder value maximization” in the 1980s, where executives were paid and evaluated based on share price performance.

This encouraged aggressive cost-cutting, reduced investment, and greater inequality. Chang notes that older forms of capitalism placed more responsibility on owners for business failure, whereas modern limited liability allows investors to take risks without carrying full consequences.

That shift made investment easier, but it also made short-term behavior more tempting. He highlights alternatives used in some countries, such as giving workers or the state a formal voice in corporate governance, to reduce the dominance of quick-return investors.

Chang then questions the claim that wages always reflect productivity. He argues that the huge wage differences between rich and poor countries are not mainly because workers in rich countries are inherently more capable or dramatically more productive.

A key reason for the gap is immigration policy. Workers in poorer countries cannot freely compete for jobs in richer ones, so the labor market is segmented by borders.

The result is that similar jobs can pay drastically different wages depending on the country, even when the difference in individual output is nowhere near that large. Chang adds that higher wages in rich countries are linked to the productivity of the most advanced firms and sectors, supported by stronger infrastructure and institutions.

In other words, a country’s overall system raises what average workers can earn, not a simple ranking of personal worth. This matters because the story that “the market pays people what they deserve” can be used to justify inequality as fair, even when the playing field is shaped by rules and history.

To counter the idea that recent technology proves the need for ever more deregulation, Chang compares the impact of the internet with household technologies like the washing machine. He argues that household appliances changed everyday life on a massive scale by reducing time-consuming labor in the home and making it easier for women to join paid work, which reshaped family structures and social expectations.

The internet improved communication and efficiency, but Chang suggests its social revolution is often exaggerated because people naturally give extra importance to what is new. He warns that overhyping certain technologies can lead to policy mistakes, such as pushing sophisticated digital solutions where basic public goods—clean water, reliable power, transport, public health—would do more to build productive economies.

Chang also disputes the view that people are motivated only by self-interest, a common assumption in market-focused models. He argues that real economies depend on trust, norms, and cooperation, not only competition and fear of punishment.

He uses examples of companies and countries where higher trust between managers and workers helped firms operate effectively and innovate. If policymakers build systems on the idea that everyone will cheat unless forced not to, they may create workplaces and institutions that encourage exactly that behavior.

Treating people as purely self-interested can become a self-fulfilling expectation, pushing out motivations like pride in work, loyalty, and concern for others.

Turning to macroeconomics, Chang challenges the claim that modern anti-inflation success made the world economy more stable. He agrees that hyperinflation can be devastating, but he argues that moderate inflation is not automatically harmful and has coexisted with rapid development in some cases.

He suggests that policies designed to keep inflation very low—often through high interest rates and strict monetary priorities—can weaken real investment, make employment less secure, and increase vulnerability to financial crises. He points to the paradox that recent decades of low inflation did not prevent major instability, including the financial crash that motivated his book.

A major theme of 23 Things They Don’t Tell You About Capitalism is that free-market policy packages rarely turn poor countries into rich ones. Chang argues that many of today’s wealthy nations used protectionism, state guidance, and selective controls during their own development.

He presents historical comparisons showing that countries now preaching open markets often had high tariffs, restrictions on foreign investment, and active industrial policy when they were catching up. From this perspective, telling developing countries to open fully and immediately is less like offering proven advice and more like pulling up the ladder after climbing it.

Chang’s argument is not that every country should close itself off, but that successful development has often required strategic sequencing: building domestic capacity before exposing fragile industries to full-scale international competition.

Chang extends this argument into globalization by insisting that “capital has a nationality.” Even when corporations operate across borders, they often keep high-value activities—especially research, design, and strategic decision-making—close to their home base. Ownership changes may shift leadership, priorities, and where investment goes.

This does not mean foreign investment is always bad, but it does mean governments should not treat transnational corporations as neutral actors whose benefits automatically flow to the host country. Developing countries, in particular, need to judge foreign investment by how it affects long-term capability: skills, technology transfer, and the growth of domestic firms.

He also challenges the popular claim that rich countries have moved beyond industry into a “post-industrial” era. Chang argues that manufacturing remains central because it is closely tied to productivity growth, technological learning, and export capacity.

Even many service jobs depend on a strong industrial base, and losing manufacturing can create persistent trade deficits that weaken a country’s position over time. Rich countries may survive such deficits longer due to currency power and financial influence, but developing countries face much sharper limits.

Chang’s warning is that skipping manufacturing is not a shortcut to prosperity; it can trap countries in lower-productivity activities with fewer pathways to catch up.

Chang then criticizes the idea that the United States automatically represents the highest living standard. He argues that living standards should be judged across a wider set of measures: inequality, health outcomes, crime, working hours, leisure, and security.

Average purchasing power can look impressive, but it may rely on conditions—such as cheap service labor tied to inequality—that lower quality of life for many workers. He suggests that comparisons based only on income per capita miss essential features of how people actually live.

On development, Chang rejects claims that Africa is destined to remain poor because of geography, climate, culture, or conflicts. He notes that many of the supposed obstacles have existed in places that later became rich and that Africa’s growth record does not support a story of inevitable failure.

He argues that external policy pressures—especially the market-opening reforms promoted by major international institutions—often constrained African governments’ ability to build industries and manage development. For Chang, the key is not to deny Africa’s challenges but to reject fatalistic explanations that excuse bad policy and remove responsibility from global economic arrangements.

One of Chang’s most direct disputes with free-market thinking is his claim that governments can sometimes pick winners. He points to cases where states fostered industries that private investors avoided because the upfront costs were high, the risks were large, and payoffs were far in the future.

He describes how coordinated government action, combined with discipline and feedback from businesses, helped certain countries build globally competitive industries. He admits that governments can fail and that some state-backed projects become expensive mistakes.

But he argues that failure also happens in private markets, and the possibility of mistakes does not prove that all government strategy is worthless. The real question is how to design institutions so that public support encourages learning, performance, and adaptation rather than permanent protection for inefficiency.

Chang also attacks the “trickle-down” claim that making rich people richer benefits everyone. He argues that the shift toward policies favoring the wealthy since the 1980s did not produce faster overall growth, and that higher inequality can reduce demand and weaken social cohesion.

He points to periods when higher progressive taxation and wider social programs coincided with strong growth. He suggests that redistribution through welfare, health, and education is not just charity; it can raise productivity and stabilize the economy by ensuring that people can participate effectively.

Money in the hands of poorer households is also more likely to circulate quickly in the real economy, supporting jobs and local businesses.

From inequality among households, Chang moves to inequality inside corporations, focusing on executive pay. He argues that the surge in CEO compensation in the United States and the United Kingdom cannot be explained by sudden leaps in managerial talent or productivity.

If top executives were truly being paid according to their contribution, he suggests, pay would not have risen so sharply in a narrow set of countries while remaining far lower elsewhere. He links inflated executive pay to power: the ability of elites to influence boards, set norms, and justify rewards even when performance is poor.

Over time, he argues, this weakens firms by diverting resources and damaging morale, while reinforcing a culture where financial engineering is valued over real improvement.

Chang then challenges stereotypes about entrepreneurship. He argues that people in poorer countries are often more entrepreneurial in the sense that many work for themselves, but this is frequently a sign of scarcity rather than dynamism.

When formal jobs are limited, people sell small goods and services to survive. He also questions whether microcredit is the miracle solution it is sometimes claimed to be, noting that small loans alone cannot create large-scale industrial capacity, advanced technology, or strong organizations.

For Chang, development depends less on heroic individual entrepreneurs and more on building systems—legal, educational, financial, and infrastructural—that allow large groups of people and firms to coordinate complex production.

A further reason Chang supports regulation is what he calls the limits of human rationality. He argues that markets are often praised for aggregating information, but individual decision-makers—whether consumers, investors, or experts—cannot fully understand complex systems.

Even highly trained professionals make systematic mistakes, and financial markets often create products so complicated that risk becomes invisible until it is too late. From this viewpoint, regulation is not a sign that officials are smarter than everyone else.

It is a practical tool for setting boundaries and preventing complexity from turning into disaster, similar to how safety testing is required in other industries where consumers cannot assess danger on their own.

Chang also questions the belief that education alone will make countries richer. He supports education for many reasons, but he argues that the connection between more schooling and higher national productivity is not as direct as commonly claimed.

Countries have grown rapidly with modest education levels, while others with relatively strong literacy have not transformed their economies. He suggests that education often functions as a screening system in labor markets, where degrees signal traits like discipline or conformity more than they provide job-specific skills.

This can lead to degree inflation, where more credentials are needed just to stand out, without a matching gain in productivity. For Chang, the decisive factor is not schooling in isolation but whether an economy creates the right kinds of jobs and industries where skills can be used and improved.

Chang tackles another common slogan: what is good for big business is good for the nation. Using examples like General Motors, he argues that firms can pursue strategies that serve their own short-term survival or profits while harming the broader economy.

Companies may demand protection instead of improving, shift from productive investment to financial activities, or seek bailouts after taking risks that impose costs on taxpayers. Chang emphasizes that national interest includes employment quality, technological capability, long-term competitiveness, and public goods.

Regulation can sometimes support those goals by discouraging behavior that sacrifices long-term strength for quick returns.

He also points out that planning did not vanish with the decline of communist systems. Governments in capitalist countries plan through budgets, industrial strategies, research funding, and public services.

Companies themselves plan constantly, setting internal targets, coordinating supply chains, and making long-term investment decisions. The real question is not whether planning exists, but who does it, for what purpose, and with what accountability.

For Chang, denying the reality of planning is a way to hide the fact that choices are being made—often by private actors whose priorities may not match the public interest.

On fairness, Chang challenges the idea that equality of opportunity is enough. He agrees that reducing legal barriers and discrimination matters, but he argues that opportunities are not meaningful when people start from radically unequal conditions.

A child cannot take advantage of schooling if they lack nutrition, safety, or stable housing. A worker cannot transition to a new industry if training and basic support are unavailable.

Chang supports targeted assistance that helps people meet basic needs so they can actually compete. He points to evidence that societies with stronger welfare systems can have higher social mobility, suggesting that a secure foundation can make opportunity more real rather than less.

Chang then argues that a “big government” welfare state can make people more open to economic change, not less. When workers have health coverage, unemployment support, and retraining options, they are less likely to fear job loss and less likely to demand protection for declining industries.

In contrast, when the safety net is weak, people cling to any job and oppose change, even when change would improve productivity overall. Chang connects this to broader economic flexibility: a secure society can adapt more easily because individuals can take risks and move across sectors without facing catastrophic consequences.

He returns to finance with a provocative claim: financial markets may need to become less efficient. By “efficient,” he means fast, liquid, and highly responsive to short-term signals.

Chang argues that such efficiency can encourage rapid trading and speculation, directing talent and capital toward financial gains rather than long-term productive investment. He describes how deregulated finance can expand credit and asset bubbles, creating instability that later harms the real economy.

Complex financial products can multiply claims on the same underlying assets, giving an illusion of wealth and safety until a shock reveals fragile foundations. Chang suggests that slowing finance—through taxes on transactions, stronger rules, and limits on certain products—can encourage longer-term thinking and reduce the risk of repeated crises.

Finally, Chang argues that good economic policy does not require elite economists alone. He respects expertise but notes that many successful development strategies were designed by people trained in law, engineering, or public administration, while many highly credentialed economists supported policies that produced weak outcomes or failed to anticipate major crises.

His point is not that expertise is worthless, but that economic decisions involve values, history, institutions, and political trade-offs. A healthy society needs informed debate among citizens, not blind trust in a single school of thought.

In the conclusion, Chang clarifies that he is not rejecting capitalism itself. He is rejecting a version of capitalism that treats corporate and financial interests as the default public interest and treats regulation and welfare as obstacles rather than tools.

He proposes principles for rebuilding a more stable and broadly beneficial economy: recognize limits in human decision-making, accept that people are motivated by more than self-interest, stop treating market outcomes as automatically fair, restore attention to real production—especially manufacturing—and bring finance back into balance with productive activity. Governments, he argues, should play an active role, and global institutions should allow developing countries the policy space to follow strategies that historically helped today’s rich nations grow.

The book ends as a call for “active economic citizenship,” where ordinary people can question slogans, examine evidence, and participate in shaping economic rules that affect everyone.

Key Figures and Metaphorical Characterizations

Ha-Joon Chang

Ha-Joon Chang functions as the book’s central voice and guiding presence rather than a character in a traditional narrative. In 23 Things They Don’t Tell You About Capitalism, he comes across as a public educator who refuses to treat economics as a closed club.

His personality on the page is shaped by a mix of skepticism and patience: he challenges popular claims, but he does so with an explanatory tone that keeps returning to first principles—what counts as “free,” who sets the rules, and who benefits. He consistently positions himself against the posture of certainty that often surrounds market fundamentalism, and he prefers arguments grounded in history, institutions, and lived outcomes over abstract models.

Chang’s “character” is built from repeated habits: questioning assumptions, showing how economic ideas become political weapons, and pushing readers toward active participation rather than passive acceptance. He also presents himself as pragmatic rather than anti-capitalist, aiming to reform capitalism by changing incentives, expanding accountability, and treating the state as a legitimate actor instead of a constant threat.

The Free-Market Economist

Although not a single individual, the free-market economist is a recurring figure in the book, serving as Chang’s main opponent in a debate that runs through the entire text. This figure represents a style of thinking that frames markets as naturally efficient, morally neutral, and self-correcting, while treating state involvement as distortion.

As a “character type,” the free-market economist is confident in tidy explanations: wages reflect productivity, shareholders discipline management, globalization lifts all boats, inflation is the core enemy, and financial liberalization improves resource allocation. Chang portrays this figure as rhetorically powerful because their claims often sound like simple common sense, yet he argues that the simplicity is achieved by ignoring institutions, power imbalances, and historical evidence.

The free-market economist also functions as a voice that turns political choices into technical necessities—calling certain rules “interference” while treating other rules as invisible and normal. In Chang’s framing, the figure is not evil or stupid; instead, it is constrained by ideology and incentives, repeatedly underestimating complexity, overpromising what competition can fix, and overlooking the costs that fall on workers, communities, and long-term industrial capability.

The Shareholder

The shareholder appears as a modern ownership figure whose power often exceeds their commitment. Chang treats shareholders as important but deeply limited stewards because many can exit easily by selling shares, which shifts their relationship to the company from responsibility to opportunity.

This mobility makes them more likely to favor strategies that boost short-term returns—even when those strategies reduce investment, weaken productivity, or damage employee morale. The shareholder becomes a symbol of an economy where control can be separated from long-term obligation, especially under limited liability, which reduces the personal downside of corporate failure.

Chang’s analysis turns the shareholder into a structural character: not a villain with a personality, but a role shaped by rules that reward quick gains and encourage pressure on managers to deliver immediate results. At the same time, Chang does not argue that shareholders should be ignored; he suggests that systems need to reduce the dominance of the most short-term-oriented owners and strengthen the influence of stakeholders who cannot simply walk away—workers, communities, and sometimes the public sector.

The Corporate Manager and CEO

Chang presents managers and CEOs as powerful decision-makers whose incentives have been reshaped by the rise of shareholder-first governance. The executive becomes a figure caught between two realities: the need to build a company that can survive and innovate over decades, and the pressure to satisfy markets that reward quarterly performance.

When pay packages and status depend on share price, executives are pushed toward tactics that look efficient on paper—cutting costs, reducing labor protections, shrinking long-term spending—while quietly undermining capabilities that take time to build, such as skill development, research capacity, and reliable supplier ecosystems. Chang also discusses executives as a class with the political and organizational power to normalize extremely high compensation, even when performance is mixed or poor.

The CEO, in this sense, represents an elite that can shape the rules of evaluation, influence boards, and defend rewards through narratives about talent scarcity. Chang’s portrait is less about individual greed and more about how executive culture and incentive design can tilt firms away from real value creation and toward financial maneuvering.

The Worker in Rich Countries

The worker in a rich country serves as an important reference point for Chang’s discussion of wages, fairness, and the myth that income automatically tracks productivity. This figure is often used to expose how borders and institutions, not just personal effort, shape economic outcomes.

Chang argues that a worker in a wealthy country may earn far more than a worker doing similar tasks in a poorer country, not because they are dramatically better at the job, but because their work is embedded in a system with advanced infrastructure, high-productivity firms, stronger bargaining contexts, and restricted labor mobility from poorer regions. The rich-country worker is also affected by policy shifts: when labor protections weaken and job insecurity rises, this worker’s confidence and willingness to adapt can decline, sometimes leading to political demands for protection that reflect fear rather than long-term economic advantage.

Chang’s treatment makes the rich-country worker a figure whose stability depends on the institutional choices that free-market ideology often wants to minimize.

The Worker in Poor Countries

The worker in a poorer country is a central moral and economic counterweight. Chang presents this figure as capable and hardworking but constrained by structures that limit productivity and bargaining power: weaker infrastructure, less access to advanced machinery and training, and reduced ability to enter high-wage labor markets due to immigration restrictions.

This worker’s low pay is therefore not proof of low worth, but evidence of unequal global arrangements and uneven national development. Chang also uses the poor-country worker to critique development strategies that rely on quick liberalization, arguing that exposure to intense international competition before domestic industries mature can trap workers in low-productivity sectors.

The figure embodies the book’s insistence that economic outcomes are not just the result of individual choices; they are the result of national capacity, policy space, and the long-term shaping of institutions.

The Domestic Worker and the Housewife

When Chang discusses technologies like the washing machine, the domestic worker and the housewife become key social figures. They represent forms of labor that are essential yet often undervalued or invisible in standard economic storytelling.

Chang argues that household technologies transformed societies by reducing the time required for domestic tasks and shifting the labor structure of households. This change reduced dependence on hired domestic servants in some contexts and made it more feasible for women to join paid work, which then altered bargaining power within families and expanded women’s public roles.

In Chang’s framing, this figure highlights how economic progress is not only about new markets or digital innovation; it also includes changes that redistribute time, reshape gender expectations, and expand who can participate in the formal economy. The domestic sphere becomes a place where economics is lived, not just measured.

The Entrepreneur in Poor Countries

Chang presents the poor-country entrepreneur as a figure often romanticized by market enthusiasts but misunderstood in practice. This entrepreneur is frequently someone pushed into self-employment by necessity rather than pulled by opportunity.

Chang portrays this character as energetic and resourceful, yet operating in crowded, low-margin spaces where many similar small businesses compete for limited demand. The entrepreneur becomes a lens for criticizing the idea that the main barrier to development is a shortage of entrepreneurial spirit.

Chang argues that what is missing is not individual hustle but the broader ecosystem that makes large-scale productivity possible—technology, institutions, coordinated investment, and stable demand. Microcredit, in this context, appears as a tool with limits: it can help some households, but it cannot substitute for industrial strategy, infrastructure, or the organizational capacity needed for complex production.

The poor-country entrepreneur thus represents both resilience and the ceiling imposed by structural constraints.

The Government Policymaker and Bureaucrat

The policymaker is one of the most contested figures, because free-market ideology often treats government actors as incompetent, self-serving, or inevitably wasteful. Chang challenges that stereotype by presenting the policymaker as a potential builder of national capability.

This figure has the power to set rules, invest in long-term projects, coordinate sectors, and protect emerging industries until they can compete. Chang’s portrayal is not naive; he acknowledges that governments can fail, pursue prestige projects, or protect inefficient firms.

What matters for him is not whether the state is automatically good, but whether institutions exist that encourage learning, discipline, and realistic assessment. The policymaker, in his account, can “pick winners” under the right conditions, especially when working closely with businesses while maintaining the authority to demand performance.

This character represents a broader argument of 23 Things They Don’t Tell You About Capitalism: that markets are structured by governance, and pretending otherwise simply hands governance to private power without public accountability.

The Development Institution and Global Policy Enforcer

Chang repeatedly invokes international organizations and global policy frameworks as an influential “character” shaping what developing countries are allowed to do. This figure appears as a rule-maker that promotes a narrow policy package—trade liberalization, deregulation, and limits on state intervention—often presented as universally valid.

Chang’s criticism is that these institutions can restrict policy space and encourage reforms that benefit global capital while leaving poorer countries with weaker tools to build domestic industries. Even when motivated by stated goals like growth and stability, the global policy enforcer becomes a force that treats countries as if they face the same starting conditions, ignoring the historical reality that today’s rich countries used protection and planning during their own rise.

Chang’s portrayal frames this character as powerful precisely because it influences national choices indirectly—through conditions, advice, and legitimacy—rather than through direct rule.

The Transnational Corporation

In Chang’s discussion, the transnational corporation is not a neutral engine of progress but a strategic actor with home-country ties. This corporate figure seeks profit and expansion across borders, but often keeps the most valuable knowledge activities—research, design, core decision-making—closer to its origin.

Chang uses ownership changes and boardroom patterns to show how national networks and preferences persist even in a global economy. The transnational corporation becomes a character that can bring jobs, investment, and skills, yet also shape a host country’s trajectory in ways that may not align with long-term national goals.

Chang’s message is that foreign investment must be evaluated by what it builds locally: capabilities, technology transfer, and domestic firms that can eventually stand on their own. This corporation is therefore both a potential partner and a potential limiter, depending on how governments negotiate, regulate, and plan around it.

The Financial Engineer and Market Trader

The financial professional appears as a symbol of a system where profit can be made faster and more easily through trading paper claims than through building products and services. Chang treats this figure as highly skilled in certain techniques but often operating inside incentives that favor complexity, speed, and short-term wins.

The creation and exchange of layered financial instruments becomes, in his account, a process that even experts can misunderstand, which increases systemic risk. The trader’s ability to move funds quickly is portrayed as both a strength and a weakness: it allows rapid responses, but it also encourages constant chasing of the best immediate return, undermining long-term investment in the real economy.

Chang’s criticism is aimed less at individual morality and more at the way deregulated finance elevates this role, rewards it lavishly, and allows it to impose costs on society when bubbles burst.

The Nobel Laureate Economist and the Overconfident Expert

Chang introduces the figure of the celebrated expert to make a broader point about the limits of human understanding. Even highly decorated economists and financial thinkers can misjudge risk, rely on fragile assumptions, and fail publicly.

This character serves as evidence against the idea that markets should be left alone because private actors supposedly have superior information. Chang argues that complex economic systems exceed anyone’s ability to model perfectly, and that expertise does not eliminate uncertainty—it can sometimes increase confidence beyond what the facts justify.

The overconfident expert represents the danger of treating economics as a predictive science that can replace public judgment. For Chang, policy should not be built on the assumption that elites will reliably foresee crises; it should be built to reduce the damage when predictions fail.

The Welfare Recipient and the Insecure Worker

Chang uses welfare recipients and workers facing insecurity as key figures in his argument about redistribution and social insurance. The welfare recipient is not portrayed as a drag on society but as a person whose support can stabilize demand and raise long-term productivity by improving access to health, education, and basic security.

The insecure worker, meanwhile, represents how fear changes economic behavior: when people worry that a job loss will ruin them, they resist change, avoid risk, and may support protection for declining industries. Chang argues that a well-designed safety net can make societies more adaptable by giving people the confidence to retrain, relocate, or accept transitions.

These figures embody his claim that social policy is not separate from economic performance; it shapes the economy’s ability to shift resources toward more productive uses without tearing communities apart.

The Citizen and Non-Economist Policymaker

The final recurring figure is the ordinary citizen—along with policymakers who are not trained economists—who Chang argues should play a central role in economic debate. This character stands against technocracy and passive acceptance.

Chang insists that economic policy involves values and trade-offs that cannot be outsourced entirely to specialists, especially when specialists can be wrong and when their preferred models can hide political choices. The citizen is therefore cast as an active economic participant: someone who questions slogans, asks who benefits, and evaluates policies by outcomes rather than ideology.

By highlighting successful policy experiences shaped by lawyers, engineers, and administrators, Chang strengthens the idea that good judgment comes from a mix of practical knowledge, historical awareness, and accountability—not only from formal economic training.

Analysis of Themes

The Myth of the Free Market

In 23 Things They Don’t Tell You About Capitalism, the idea of the “free market” is treated not as an economic fact but as a political construction. The book argues that markets never exist in a vacuum; they are always structured by laws, norms, and institutional decisions that define what is allowed, who can participate, and how disputes are resolved.

By pointing to examples such as child labor laws, restrictions on bribery, and financial regulations, the text shows that what counts as “freedom” in a market depends on collective judgments that evolve over time. Activities that once seemed normal can later be considered unacceptable, which reveals that markets are shaped by moral and social choices rather than operating according to neutral, natural laws.

This theme challenges the rhetorical power of labeling certain policies as “interference.” When regulations are presented as distortions of an otherwise pure system, the underlying assumption is that there exists a baseline condition of total freedom. The book disputes that baseline.

It insists that even the most market-oriented economies rely on strong property rights, contract enforcement, central banking, and legal frameworks—all forms of structured governance. By exposing this, the text shifts the debate from whether there should be regulation to what kind of regulation should exist and whose interests it serves.

The broader implication of this theme is democratic. If markets are always governed, then economic arrangements are not fixed truths but collective choices.

Citizens therefore have a legitimate role in debating how markets are structured. The myth of the free market functions to narrow that debate by suggesting that any deviation from a particular model is irrational or inefficient.

By rejecting that myth, the book reopens space for alternative policies and emphasizes that economic rules are not sacred but subject to revision.

The Limits of Market Rationality

A sustained concern is the exaggerated faith in market rationality. The text questions the assumption that individuals and firms always make decisions that maximize long-term efficiency or social benefit.

It draws attention to the concept of bounded rationality, arguing that people operate with incomplete information and limited cognitive capacity. In complex systems—especially financial markets—this limitation becomes especially dangerous.

Even highly trained experts can misjudge risk, misunderstand new instruments, or rely too heavily on models that simplify reality.

This theme is reinforced through discussions of financial crises and speculative behavior. The book presents the idea that markets are prone to herd dynamics, short-term thinking, and overconfidence.

When financial assets can be traded quickly and profitably, actors may prioritize immediate gains rather than sustainable investment in production. This behavior is not necessarily irrational at the individual level; it can be a rational response to incentives.

However, when everyone responds to the same short-term signals, the system as a whole becomes unstable.

By questioning the infallibility of markets, the book also questions the claim that government actors are uniquely irrational. If private decision-makers can miscalculate and create systemic risks, then the argument for leaving markets entirely alone weakens.

Regulation becomes not a sign of superior wisdom but a tool to manage complexity and reduce harm. The theme ultimately reframes economic governance as a response to human limitation rather than an intrusion into perfect self-regulation.

The Political Nature of Economic Policy

Throughout the text, economic policy is portrayed as deeply political rather than purely technical. Policies about trade, taxation, welfare, corporate governance, and finance are often presented as matters of efficiency, but the book argues that they reflect choices about power, distribution, and long-term priorities.

Labeling a policy as “pro-market” or “anti-market” can obscure whose interests are being advanced and whose are being constrained.

The historical comparisons used in the text highlight this political dimension. Wealthy countries that now advocate open markets frequently relied on protectionism, state support, and strategic intervention during their own development.

This suggests that today’s global rules are not the natural outcome of economic evolution but the result of negotiations shaped by existing power hierarchies. When developing countries are told to liberalize quickly, they are often operating under constraints that richer countries did not face at comparable stages.

The theme extends to domestic debates as well. Decisions about whether to prioritize shareholder value, how to structure executive compensation, or how generous to make welfare systems are not dictated by immutable economic laws.

They are the outcome of bargaining, ideology, and institutional design. By making this explicit, the book challenges the tendency to treat market-oriented reforms as inevitable.

Economic policy, in this view, is a field of contestation, where different visions of fairness, stability, and growth compete.

Inequality and the Distribution of Rewards

Inequality is treated as a structural outcome of institutional design rather than as a simple reflection of merit. The book disputes the belief that wages and incomes naturally align with individual productivity.

Differences in national infrastructure, immigration policies, bargaining power, and corporate governance all influence how rewards are distributed. The book argues that extreme inequality, especially when driven by executive pay structures and pro-rich tax policies, can undermine both fairness and long-term growth.

The discussion of shareholder value and CEO compensation illustrates how institutional changes can amplify inequality. When executive pay becomes tied to short-term share price, and when tax systems favor capital gains and high incomes, wealth accumulates at the top without necessarily increasing productive investment.

This dynamic contradicts the argument that enriching the wealthy will automatically generate widespread prosperity. Instead, the book suggests that concentration of income can reduce aggregate demand and weaken social cohesion.

The theme also addresses global inequality. Wage differences between countries often reflect restricted labor mobility and uneven development rather than inherent differences in ability.

By highlighting these systemic factors, the text undermines narratives that justify inequality as the fair outcome of competition. Redistribution, social insurance, and public investment are presented not as moral indulgences but as mechanisms that can support productivity and stability.

Inequality, therefore, is not an inevitable byproduct of efficiency but a choice embedded in policy.

The Role of the State in Economic Development

The state appears as a central actor in shaping economic trajectories. Contrary to the view that governments should merely enforce contracts and protect property rights, the book argues that public institutions have historically played active roles in fostering industry, funding research, and coordinating long-term investment.

Examples from various countries illustrate how strategic intervention helped build competitive sectors that private capital alone might have avoided due to risk or delayed returns.

This theme also addresses the criticism that governments cannot “pick winners.” While acknowledging that public projects can fail, the text points out that private markets also generate costly failures. The question is not whether mistakes occur but how learning and accountability are structured.

Successful state interventions often involve close communication with industry, performance standards, and a willingness to withdraw support when firms underperform. The book suggests that dismissing all state involvement because of potential inefficiency ignores a substantial historical record of effective collaboration.

The broader implication is that development requires coordinated action that markets alone may not provide. Infrastructure, education systems aligned with industrial needs, technological research, and temporary protection for emerging industries can create conditions for sustained growth.

By reframing the state as a builder of capacity rather than merely a regulator, the theme challenges minimalist conceptions of governance and supports a more balanced partnership between public and private sectors.

Financialization and Economic Instability

A critical theme concerns the expansion of financial activities relative to the real economy. The text argues that when profits become easier to generate through trading financial assets than through producing goods and services, incentives shift in ways that can destabilize the system.

Financial markets are praised for liquidity and speed, yet these same qualities encourage rapid shifts in capital that amplify booms and busts.

The book analyzes how deregulation and innovation in financial instruments can create layers of complexity that obscure risk. Mortgages, derivatives, and other products multiply claims on underlying assets without increasing real productive capacity.

When confidence falters, these interconnected claims unravel quickly, spreading losses across institutions and borders. The crisis that frames the book’s publication is presented as evidence that highly “efficient” financial markets can be fragile.

This theme also addresses the cultural shift that accompanies financialization. Corporate strategies increasingly prioritize financial engineering over investment in skills, research, and production.

Talented individuals may gravitate toward finance because it offers higher returns, potentially diverting expertise from sectors that build long-term capacity. The book argues for measures that slow down speculative flows and redirect attention to sustainable investment.

Stability, in this view, requires recognizing that finance should serve production rather than dominate it.

Development, Manufacturing, and Structural Transformation

The importance of manufacturing and structural transformation runs throughout the discussion. The text disputes the claim that countries can leap directly into service-based or knowledge-driven economies without building industrial capacity.

Manufacturing is portrayed as crucial not only for exports but for learning, technological upgrading, and productivity growth. Industrial sectors often generate spillovers that strengthen related activities and improve overall efficiency.

The argument extends to trade policy and globalization. Developing countries that open their markets prematurely may struggle to compete with established firms from richer nations.

Without time and support to build domestic industries, they risk becoming dependent on low-value activities or raw material exports. The book emphasizes that today’s wealthy countries often protected and nurtured their industries during earlier stages, suggesting that strategic sequencing matters.

Structural transformation is presented as a complex, long-term process involving coordination among firms, workers, and the state. Education, infrastructure, and industrial policy must align with realistic goals and capacities.

The theme underscores that development is not automatic; it requires deliberate choices about which sectors to prioritize and how to integrate into the global economy. By challenging the notion that services alone can drive prosperity, the book reinforces the importance of tangible production and technological depth.

Welfare, Security, and Economic Flexibility

Social welfare is reframed as a contributor to economic dynamism rather than an obstacle to it. The text argues that when individuals have access to healthcare, unemployment benefits, and retraining programs, they are less fearful of change.

This security can make workers more willing to move between jobs, accept restructuring, or acquire new skills. In contrast, weak safety nets may lead people to resist change, even when change would improve productivity in the long run.

The theme connects welfare policy to political stability and social mobility. Assistance targeted at basic needs can help level starting conditions, making opportunity more substantive rather than merely formal.

By supporting education, health, and income stability, welfare systems can enhance human capital and broaden participation in economic life. The book points to evidence that some countries with extensive social programs have maintained strong growth and adaptability.

This perspective challenges the assumption that redistribution inevitably reduces incentives. Instead, the text suggests that well-designed systems can balance support with accountability.

The broader argument is that economic flexibility depends not only on deregulation but also on trust and security. When citizens feel protected from catastrophic loss, they may support reforms that would otherwise appear threatening.

Welfare, therefore, becomes part of the architecture of a resilient economy rather than a drain on it.