The Art of Spending Money Summary and Analysis

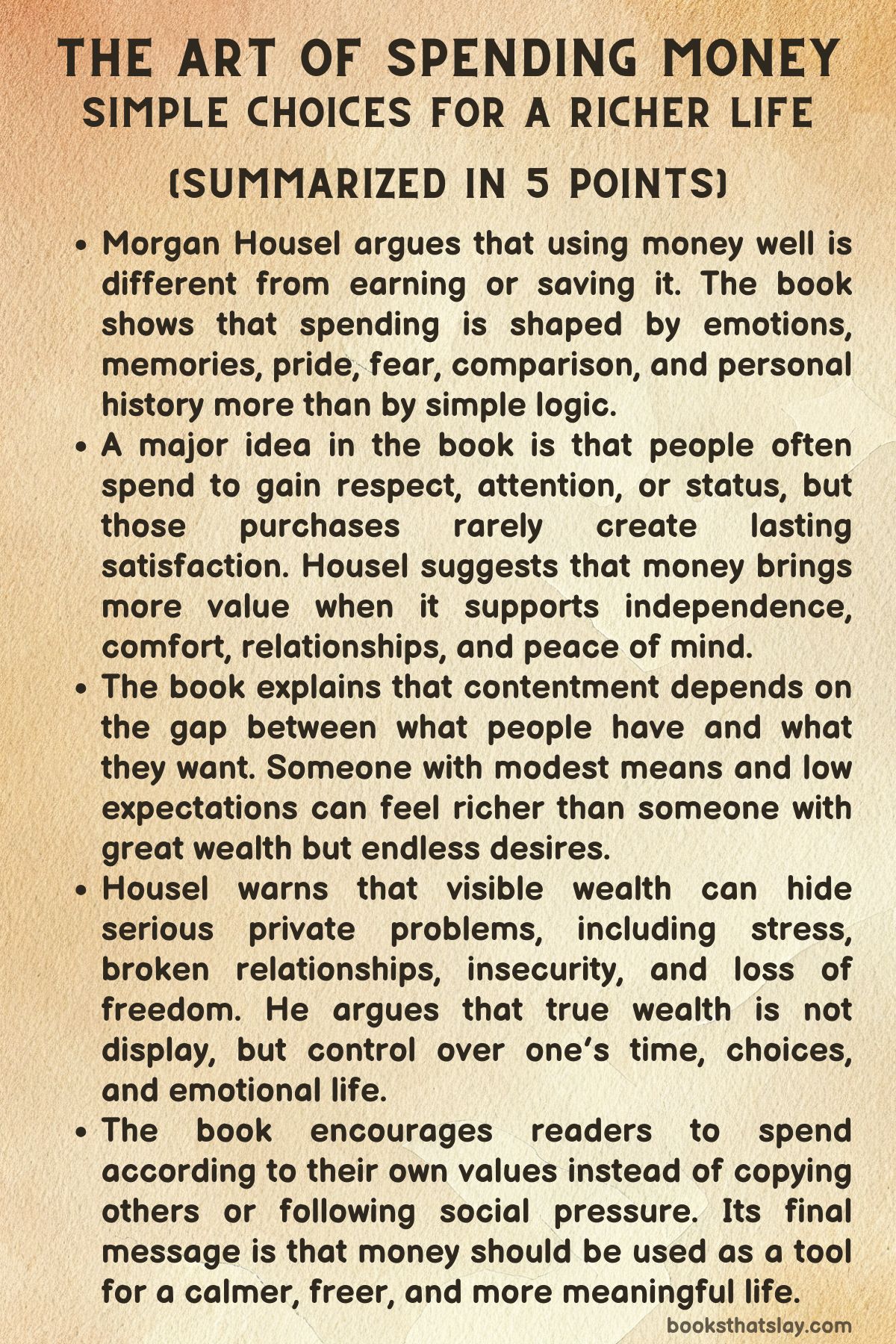

The Art of Spending Money by Morgan Housel is a nonfiction book about the emotional side of money. Housel argues that earning money and using it well are separate skills, and that most spending choices are shaped less by logic than by memory, insecurity, comparison, status, family pressure, fear, and hope.

Rather than offering rigid budgeting rules, the book asks readers to understand what they truly want money to do for them. Its central idea is simple but demanding: money works best when it buys independence, calm, meaning, and contentment instead of applause.

Summary

The Art of Spending Money begins with the idea that money is not mainly a mathematical subject. Housel argues that people can be excellent at earning, saving, or investing and still be poor at using money in ways that improve their lives.

The central problem is that money carries emotional weight. It represents safety, identity, attention, freedom, family duty, revenge against past hardship, and the desire to prove oneself.

Because of this, financial behavior often looks irrational from the outside but makes sense when a person’s background is understood.

Housel opens by challenging the assumption that wealth naturally leads to happiness. He recalls seeing a wealthy man buy an extremely expensive armchair largely because he believed this was the sort of thing rich people were supposed to buy.

That moment reveals one of the book’s core concerns: many people spend not from genuine desire but from a script written by class expectations, social comparison, and status anxiety. Money can serve a person, but it can also become a quiet master, telling them what to want and how to measure themselves.

The book then explains that all spending behavior becomes more understandable with enough information. One person may overspend because childhood poverty left them needing visible proof that they escaped scarcity.

Another may under-spend because financial trauma taught them that safety can disappear at any moment. High-earning professionals may spend recklessly after long, stressful work periods because they feel the need to compensate themselves for exhaustion.

Housel’s point is not that every choice is wise, but that financial behavior is personal. A purchase that looks foolish to one person may satisfy a deep emotional need for another.

From there, Housel turns to the hunger for attention. People often believe they want a luxury car, a bigger house, or an impressive object, but what they really want is respect.

The problem is that material objects rarely create the kind of respect people crave. They may attract brief attention from strangers, but they do not make loved ones admire someone’s character.

Housel separates external validation from internal satisfaction. A life built around impressing others becomes unstable because public approval is temporary, competitive, and never fully controllable.

A major part of the book is devoted to contentment. Housel presents happiness as the gap between what people have and what they want.

Someone with modest resources and modest desires can feel richer than a billionaire whose expectations keep expanding. He uses examples of people who lived with little yet felt deeply satisfied, contrasting them with extremely wealthy people who still felt restless.

The book argues that the human brain often enjoys anticipation more than possession. Once a goal is reached, the mind quickly searches for the next one.

Without contentment, more money only creates more appetite.

Housel also warns that people see only the visible side of wealth. They see mansions, cars, travel, and expensive purchases, but not loneliness, family conflict, depression, addiction, divorce, or stress.

This hidden side matters because people often imagine money will improve every part of life, when in reality it has limits. Money can make a good life more comfortable, but it cannot automatically create love, health, purpose, trust, wisdom, or emotional stability.

If these foundations are missing, wealth may magnify problems rather than solve them.

The book repeatedly returns to the idea that the most valuable financial asset is not needing to impress anyone. Housel uses the story of Donald Crowhurst and Bernard Moitessier to show two opposing relationships with recognition.

Crowhurst, driven by public validation, becomes trapped in fraud and despair during a sailing race. Moitessier, who could have won, abandons the race because winning no longer matches his deeper values.

Their contrast shows how external approval can become dangerous, while inner independence allows a person to walk away from applause.

Housel then explores the difference between being rich and being wealthy. Being rich means having money to buy things.

Being wealthy means controlling how money affects one’s freedom, personality, relationships, morals, and mental health. The Vanderbilt family becomes a warning.

Their enormous fortune faded as heirs became consumed by status, competition, and expensive obligations. By contrast, Chuck Feeney, who gave away nearly all of his fortune and lived simply, becomes an example of someone who controlled money rather than being controlled by it.

The book suggests that true wealth lies in command over desire.

Another key distinction is utility versus status. Utility means buying something because it genuinely improves life.

Status means buying something to shape how others see you. Housel argues that utility produces more lasting satisfaction because it is rooted in real use, comfort, and personal preference.

Status is fragile because it depends on trends and other people’s reactions. A person buying for utility may choose comfort, reliability, and quiet enjoyment.

A person buying for status may spend more and enjoy less because the purchase is aimed outward rather than inward.

The book also deals with regret. Housel says good financial decisions require imagining how today’s choices will feel years later.

Excessive saving can lead to regret if it sacrifices too much life, family, and experience. Reckless spending can lead to regret if it destroys future freedom.

He criticizes both extreme deprivation and extreme impulsiveness. A wise financial life balances present joy with future flexibility.

Saving, in his view, is not merely delayed consumption. It buys immediate independence, reduced stress, options, and dignity.

Social comparison becomes another major danger. Housel argues that envy turns personal finance into a competition no one can win.

People compare their private worries to other people’s public displays, especially in a world shaped by social media. The result is dissatisfaction, debt, and poor judgment.

A person’s chosen peer group can quietly define what feels normal, luxurious, embarrassing, or necessary. For Housel, financial independence is partly freedom from this comparison trap.

The book then reframes savings as the purchase of independence. Housel compares people who earned vast sums but lost control of their lives with people who earned less but protected their freedom.

The message is that wealth without autonomy is a form of poverty. Debt, lifestyle inflation, and constant obligations can make even high earners dependent on employers, creditors, or social expectations.

Every dollar saved can move a person toward greater control over time and choice.

Housel also introduces social debt, the hidden burden created when spending attracts judgment, obligation, envy, or pressure. Public displays of wealth can make people targets.

Lottery winners, athletes, and wealthy families may face endless requests, resentment, and expectations. Even ordinary purchases can create social debt if they force someone to maintain an image.

Privacy, modesty, and restraint become valuable because they protect freedom.

Later sections focus on patience, identity, experimentation, family, emotion, and small expenses. Housel praises quiet compounding: building wealth slowly without public attention.

He warns against turning financial habits into identity labels, because a person who becomes “a saver” or “a certain kind of investor” may lose the flexibility to change. He encourages experimentation with spending, arguing that people should try different uses of money and keep only what genuinely improves life.

When discussing children, Housel argues that parents teach money values more through behavior than lectures. Children absorb attitudes about envy, gratitude, fear, work, generosity, and status from daily observation.

Parents who preach frugality while living lavishly create resentment. The better legacy is not just money but confidence, emotional security, empathy, and resilience.

The book also insists that spreadsheets cannot capture everything. Some purchases matter because of memories, family meaning, emotional comfort, or personal peace.

The best money choices combine rational boundaries with emotional truth. Housel does not reject math; he rejects the idea that math alone can define a good life.

Near the end, Housel examines greed and fear as a repeating cycle. Success can make people overconfident, which leads to bigger risks, denial, loss, and then fear.

After suffering, people may believe they have earned wisdom, which can set up the next round of overconfidence. The book closes by identifying behaviors that make people miserable with money: comparison, status chasing, rigid beliefs, ignoring hidden costs, treating money as either everything or evil, and forgetting the role of luck.

Housel’s final message is one of humility. The luckier and more prosperous someone becomes, the kinder and more grounded they should be.

Key Figures

Morgan Housel

Morgan Housel functions as the guiding voice of the book rather than as a detached financial instructor. He writes from the position of someone interested in behavior, memory, pride, fear, family, and daily peace, not just in budgets or investment returns.

In The Art of Spending Money, he presents himself as a person who values simplicity, savings, low debt, and independence, but he does not turn his own habits into universal law. His strength as the central figure is that he recognizes how varied people’s financial needs can be.

He uses his own life carefully, especially when discussing his home, his family, and his preference for calm over maximum income. Housel’s character is analytical but not cold.

He respects numbers, yet he keeps returning to the emotional reason behind every number. His role is to move readers away from shame and comparison and toward self-knowledge.

The Wealthy Man with the Armchair

The wealthy man who buys the expensive armchair becomes an early symbol of status-driven spending. He is important because he shows that wealth does not automatically create clarity.

His purchase is not presented as a simple love of furniture; it becomes a sign of a person trying to perform wealth according to an imagined standard. He seems to believe that being rich comes with certain obligations, including buying objects that confirm his place in a social class.

In the book, he represents the danger of letting money follow expectation instead of preference. His choice is not tragic in a dramatic sense, but it is revealing.

It shows how easily people can lose contact with their own desires once they begin asking what someone in their position is supposed to own.

Tiffany Aliche

Tiffany Aliche appears as a figure shaped by financial trauma. Her difficulty with spending is not treated as irrational stinginess but as the result of a past experience that made money feel fragile.

She represents people who cannot easily enjoy what they have because earlier hardship trained them to expect loss. Her character is important because she complicates the idea that the best financial behavior always looks like confidence, generosity, or comfort with spending.

Sometimes restraint is not just discipline; it is self-protection. Through her, the book argues that financial habits are often emotional survival strategies.

Aliche’s example also supports Housel’s broader claim that outsiders should be careful before judging someone else’s money choices, because the visible action rarely contains the full story.

The Investment Bankers

The investment bankers in the book represent high earners whose spending is tied to exhaustion and compensation. Their behavior may look careless from the outside, but Housel uses them to show that spending can become a way to recover emotionally from intense work.

They are not simply people with too much money and too little judgment. They are figures caught in a cycle where stress creates the desire for reward, and reward often takes the form of expensive consumption.

Their role is to show how money can become a pressure valve. In this sense, they reveal a hidden cost of demanding careers: the salary may be high, but the emotional bill often arrives through lifestyle inflation, impulsive purchases, and the need to justify long hours.

Housel’s Grandmother-in-Law

Housel’s grandmother-in-law is one of the book’s clearest examples of contentment. She lives with very little by conventional standards, yet she is described as deeply happy because her expectations are aligned with her circumstances.

Her importance comes from the way she reverses ordinary assumptions about wealth. She may not possess much money, but she has something many rich people lack: enoughness.

In the book, she shows that happiness is not determined only by income or possessions but by the distance between desire and reality. Her character quietly challenges consumer culture.

She does not need to win a financial race because she is not running one. Through her, Housel presents contentment as a form of wealth that cannot be bought after the fact.

J. Paul Getty

J. Paul Getty appears as a warning that extreme wealth does not guarantee emotional ease. As one of the richest people in the world, he had the kind of fortune many people imagine as a cure for worry, envy, and sadness.

Yet Housel uses him to show that money cannot purchase a cheerful temperament or heal every internal condition. Getty’s significance lies in the contrast between public success and private dissatisfaction.

He forces readers to question the fantasy that a larger bank account will automatically change the emotional texture of daily life. In the book, Getty is not presented mainly as a financial giant but as evidence that wealth leaves many human problems untouched.

Donald Crowhurst

Donald Crowhurst is one of the most tragic figures in the book because his need for validation traps him. He enters the sailing race without the preparation, experience, or vessel required for the challenge, and when failure becomes clear, he chooses deception rather than public embarrassment.

His story shows the destructive power of external benchmarks. Crowhurst is not ruined only by the sea; he is ruined by the imagined judgment of others.

In The Art of Spending Money, he represents what can happen when identity depends too heavily on public success. His choices become increasingly desperate because admitting the truth would destroy the image he hoped to create.

Through him, Housel turns the need to impress into a serious moral and psychological danger.

Bernard Moitessier

Bernard Moitessier stands opposite Crowhurst. He has the skill and position to win the race, yet he abandons it because victory no longer fits his deeper sense of purpose.

His character matters because he shows what independence looks like in action. He is not indifferent because he lacks ambition; he is free because he can reject a prize that no longer serves him.

In the book, Moitessier becomes a model of internal measurement. He values sailing, simplicity, and personal meaning more than public recognition.

His decision to continue toward Tahiti instead of finishing the competition shows that real wealth can mean having the courage to disappoint spectators in order to remain loyal to oneself.

The Vanderbilt Family

The Vanderbilt family serves as a large-scale example of money losing its usefulness because it becomes attached to status, rivalry, and identity. Cornelius Vanderbilt creates a vast fortune, but later generations struggle to preserve either the money or the values that might have protected it.

The family’s mansions, yachts, collections, and social competition show how wealth can turn into lifestyle debt. Their story is not simply about bad spending; it is about a family allowing money to define importance.

Reginald Claypoole Vanderbilt’s decline and George Washington Vanderbilt’s grand but impersonal Biltmore House both reveal how abundance can fail when it lacks purpose. In the book, the Vanderbilts warn that being rich is not the same as being free.

Chuck Feeney

Chuck Feeney is one of Housel’s strongest examples of a person who controls money rather than being controlled by it. Although he amasses a huge fortune, he eventually gives nearly all of it away and keeps a comparatively modest amount for himself and his wife.

His character is powerful because he experiments with luxury, finds it unsatisfying, and then changes course. He does not reject money; he uses it according to his values.

Feeney’s simple living, coach flights, modest apartment, and philanthropy show that wealth can be transformed into purpose when the owner is not seeking applause. He represents a mature form of financial success: knowing what is enough, knowing what matters, and acting on that knowledge.

Bill Koch

Bill Koch appears in the discussion of utility and status through his purchase of rare wines that later turn out to be counterfeit. His disappointment is revealing because the pleasure of the wine itself is not the main issue.

What collapses is the status attached to rarity, authenticity, and ownership. Koch’s role in the book is to show that some purchases derive much of their value from the story around them.

When the story is false, the object loses its emotional power even if its practical qualities remain similar. He becomes an example of how status spending depends on fragile external meanings.

The lesson through him is not that collecting is foolish, but that people should understand what kind of satisfaction they are actually buying.

Michael May

Michael May’s experience after regaining sight gives the book one of its clearest examples of contrast as a source of joy. When he sees ordinary things with wonder, his reaction shows that happiness often comes not from the objective value of an item or experience but from the gap between before and after.

His character matters because he sees what others overlook. A carpet can become astonishing when it arrives after years without sight.

In the book, May represents fresh perception. He reminds readers that luxury often fades when it becomes normal, while simple things can create great joy when viewed from a different baseline.

His story supports Housel’s argument for protecting contrast rather than endlessly raising expectations.

Ernest Shackleton’s Crew

The crew from the Shackleton expedition represents gratitude created by hardship and contrast. Their long period of deprivation makes ordinary comforts feel extraordinary when they return to safety.

Warmth, food, bathing, and shelter become powerful not because they are rare luxuries in ordinary life, but because the crew has lived without them. Their role in the book is not to romanticize suffering but to show how appreciation is shaped by experience.

They make clear that constant comfort can dull the senses, while scarcity can restore the emotional value of basic things. Housel uses them to argue that a simpler baseline can make occasional comforts more meaningful.

Antoine Walker

Antoine Walker represents the danger of high income without independence. His NBA earnings are enormous, yet lavish spending, real estate, cars, and obligations to others eventually lead to bankruptcy.

He is important because his story breaks the assumption that earning a fortune is the same as securing freedom. In the book, Walker becomes a figure of lost autonomy.

His money initially expands choice, but his spending patterns and social obligations eventually narrow it. His life shows that wealth can disappear when it is treated as proof of status or as an unlimited resource for every demand.

Walker’s character reminds readers that financial success without boundaries can end in dependence.

John Urschel

John Urschel is placed in contrast with Antoine Walker. He earns far less as a professional athlete but saves enough to step away from football and pursue a PhD at MIT.

His character represents independence as the highest financial achievement. He does not need the largest income to be the stronger example; he needs enough control to choose his next life.

In the book, Urschel shows that money’s best use may be to make a person less trapped. His story is built around option value, discipline, and a clear sense of personal direction.

He demonstrates that success should not be measured only by earnings but by the freedom those earnings create.

Frank Lucas

Frank Lucas appears as a dramatic example of social debt. His decision to wear an expensive chinchilla coat attracts attention that contributes to his downfall.

In the book, he represents the danger of public display. The coat is not just clothing; it is a signal that changes how others see him and how authorities respond to him.

Housel uses Lucas to show that visibility can become a liability. Money spent to be noticed may create consequences that far exceed the purchase price.

His character reveals that privacy has financial and personal value. Sometimes the most expensive thing a person can buy is attention.

Parents and Children

Parents and children function as a shared character group because the book treats family as one of the most powerful settings for financial behavior. Parents shape children less through speeches than through repeated signals: how they react to raises, losses, bills, neighbors, luxuries, work, and envy.

Children learn what money means by watching whether adults treat it as safety, status, control, fear, generosity, or love. In The Art of Spending Money, this relationship becomes morally significant because parental choices can create confidence or pressure.

When parents give too much, they may weaken ambition. When they give too little or act hypocritically, they may create resentment.

The best inheritance, Housel suggests through this group, is emotional security and strong values rather than mere assets.

Jason Zweig’s Mother

Jason Zweig’s mother appears in the discussion of emotional value. Her difficulty in selling her longtime home shows why some financial choices cannot be reduced to market price.

A house can be valued by square footage, location, and resale potential, but it can also contain memories that no spreadsheet can measure. Her character is important because she gives dignity to emotional attachment.

The book does not mock her hesitation; instead, it uses her to show that rational finance must leave room for human meaning. She represents the difference between what something is worth in money and what it is worth in memory.

Calvin Coolidge

Calvin Coolidge appears as an example of attention to small expenses. His frugality, including concern over government stationery and pencil use, can seem excessive at first.

Yet Housel uses him to show that small costs can matter when repeated at scale. Coolidge’s character represents discipline, restraint, and respect for accumulated impact.

He also helps set up the book’s balanced view: small expenses should not distract from major decisions, but they should not be dismissed either. Through Coolidge, Housel shows how carefulness can be rational when the scale is large enough.

He becomes a symbol of the compounding power of minor choices.

Kevin Costner and Michael Blake

Kevin Costner and Michael Blake appear together in a story about status, humility, and the danger of judging people by their current circumstances. Costner initially dismisses Blake, who is struggling financially, but Blake’s writing later becomes the basis for a major artistic and commercial success.

Their relationship matters because it shows that wealth and present status are poor measures of human potential. Costner’s early attitude represents the blindness that success can create, while Blake represents overlooked value.

The book uses their story to argue that financial luck should make people kinder, not more dismissive. Their example broadens the book’s financial message into a moral one: never confuse someone’s bank balance with their worth.

Themes

Money as Independence

Money’s highest use is the purchase of independence: control over time, decisions, work, relationships, and daily stress. Housel repeatedly argues that savings should not be viewed only as postponed pleasure.

Every saved dollar gives a person more room to breathe in the present. It can make it easier to leave a bad job, handle an emergency, avoid humiliating dependence, support a family choice, or say no to obligations that violate personal values.

This theme changes the meaning of wealth. Instead of defining wealth as visible consumption, the book defines it as freedom from being cornered.

A person who earns a great deal but must keep working under pressure to support debt, status, and expectations may be less free than someone with modest income and strong control over spending. This is why Housel admires figures who use money to protect calm and choice rather than to signal rank.

In The Art of Spending Money, independence becomes a practical and emotional asset. It is practical because it creates options, and emotional because it reduces fear.

The theme asks readers to treat freedom as something worth buying before luxury.

The Trap of Status

Status spending is shown as one of the most common ways people lose contact with their own happiness. The desire to be admired is human, but Housel argues that material objects rarely provide the respect people actually want.

A luxury purchase may draw attention, yet attention is not the same as love, trust, or lasting admiration. This theme appears through the expensive armchair, the comparison between utility and status, the Vanderbilt family, Bill Koch’s rare wines, social media envy, and Frank Lucas’s coat.

Status is unstable because it depends on other people’s reactions, and those reactions change quickly. What impresses one group today may become ordinary tomorrow.

Even worse, status spending often creates new obligations. A person who buys an image must maintain it, defend it, upgrade it, and worry about losing it.

Housel does not deny that humans care about belonging, but he warns that seeking belonging through objects can become expensive and hollow. The healthier alternative is self-knowledge: spending on what genuinely improves life, even when it is unimpressive to others.

Status asks, “What will they think?” Utility asks, “Will this make my life better?”

Contentment, Expectations, and Contrast

Contentment in the book depends less on what a person owns than on what a person expects. Housel’s happiness equation is built around the gap between possessions and desires.

If desires grow faster than resources, dissatisfaction continues no matter how much money arrives. This theme explains why modest lives can be rich in satisfaction and wealthy lives can remain restless.

It also explains why luxury loses power when it becomes routine. The first upgrade feels wonderful because it creates contrast; the tenth upgrade may barely register because expectations have already adjusted.

Michael May’s joy at seeing ordinary surroundings and the Shackleton crew’s gratitude for basic comforts both show how perception is shaped by prior experience. Housel’s argument is not that people should seek hardship or deny themselves all pleasure.

Instead, he suggests that a lower baseline can preserve appreciation. Occasional luxuries become more enjoyable when they remain occasional.

This theme challenges lifestyle inflation, where every raise quietly becomes a new normal. Contentment requires managing desire, not just increasing income.

The person who wants less gains a kind of wealth that cannot be matched by endless acquisition.

Humility, Luck, and Emotional Honesty

Financial wisdom in the book requires humility about luck and honesty about emotion. Housel repeatedly challenges the belief that success is always earned and failure is always deserved.

People tend to credit their own victories to skill while blaming their losses on circumstances, then reverse that judgment when looking at others. This distorted thinking leads to arrogance, envy, harsh judgment, and poor decisions.

The theme appears strongly in the final discussion of kindness: the luckier someone becomes, the more respectful and generous they should be toward others. Humility also matters because financial choices are not purely rational.

Homes, family memories, fear, identity, pride, regret, and childhood experience all influence money decisions. A spreadsheet may calculate price, but it cannot fully measure comfort, meaning, or peace.

Housel asks readers to acknowledge those emotions rather than pretend they do not exist. Emotional honesty does not mean reckless spending.

It means building financial choices inside reasonable limits while admitting what truly matters. This theme gives the book its humane quality.

Money is not only a tool of calculation; it is also a mirror that reflects fear, hope, ego, gratitude, and love.