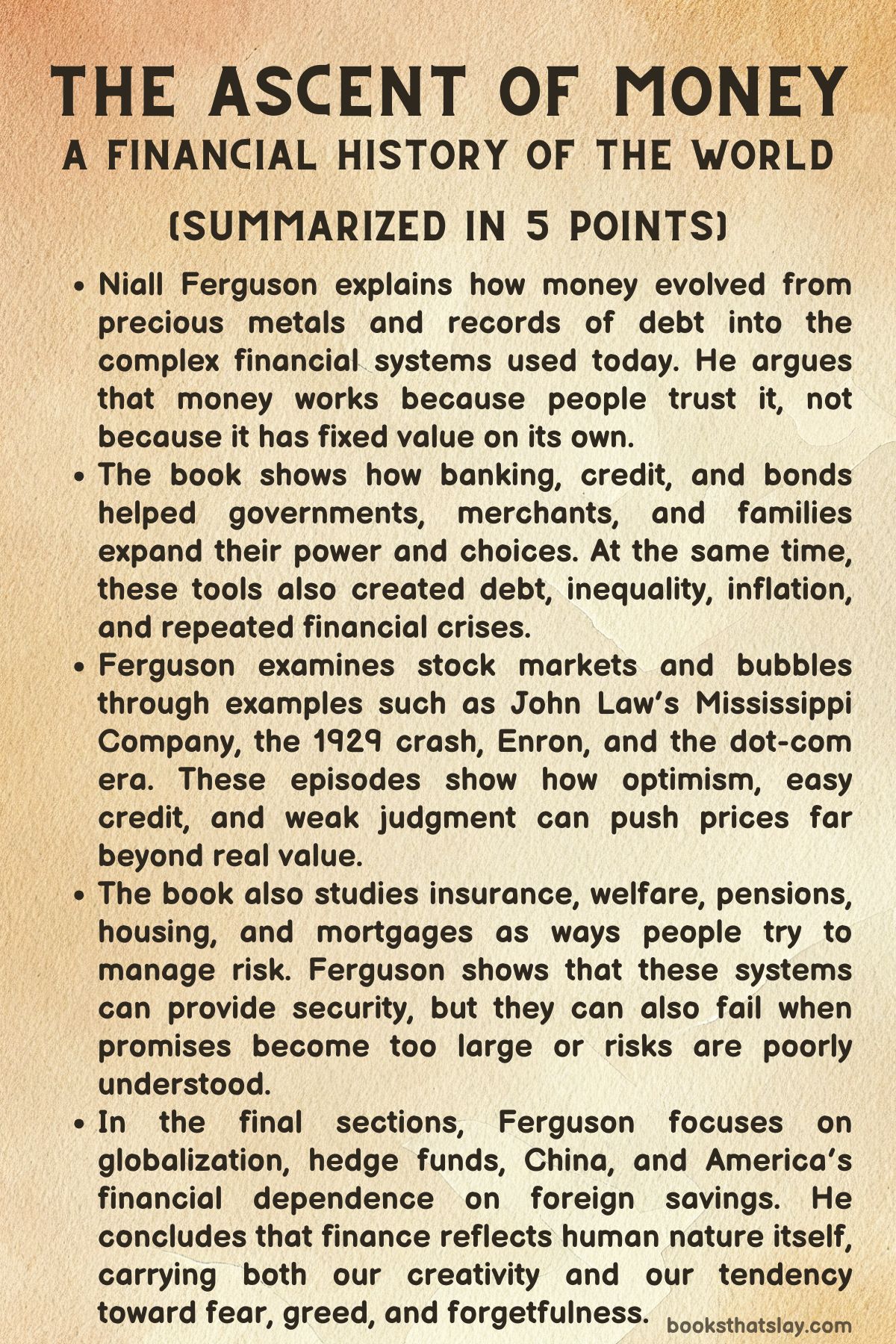

The Ascent of Money Summary and Analysis

The Ascent of Money: A Financial History of the World by Niall Ferguson is a history of finance that treats money not as a dry technical subject, but as one of the forces that shaped civilization. Ferguson explains how coins, banks, bonds, stock markets, insurance, property, and global capital flows changed the way people live, fight, build, borrow, and take risks.

The book argues that financial innovation has mattered as much as technological innovation in human progress. It also warns that every financial system reflects human nature: ambition, fear, greed, trust, memory, and error.

Summary

The Ascent of Money begins with a central claim: money is not just a tool of trade, but one of the hidden engines of history. Ferguson starts by pointing out that modern life is surrounded by financial language, institutions, and habits, even though many people understand little about how they work.

The world’s richest bankers and hedge fund managers seem far removed from ordinary earners, yet their activities are linked to the same financial system that shapes mortgages, pensions, credit cards, savings, jobs, and government spending. The book argues that resentment toward financiers has deep roots, partly because debtors usually outnumber creditors, crises seem to expose the cruelty of finance, and minority groups have often been pushed into money-lending roles.

Still, Ferguson’s central argument is that financial development has helped civilization advance.

The story begins with the origins of money itself. Ferguson contrasts societies that had precious metals but no money economy with European conquerors who understood gold and silver as wealth.

The Spanish conquest of the Inca Empire shows that metal alone does not create prosperity. Spain gained vast quantities of silver from the Americas, especially from mines worked through forced labor, but too much silver lowered its value and helped create inflation.

The lesson is that money is not valuable simply because it is made of precious material. It depends on trust, scarcity, and the belief that others will accept it in exchange.

This idea connects ancient clay tablets, metal coins, paper notes, and modern electronic transactions: all money relies on shared confidence.

From money, Ferguson moves to credit and banking. Credit allows people to act before they have cash in hand, but it also creates obligations and risk.

Northern Italy becomes a key setting because its city-states developed sophisticated lending practices. Fibonacci’s introduction of Hindu-Arabic numerals to Europe made calculation easier and helped merchants and lenders manage interest, debt, and profit.

Venice and Florence show how money-lending became both useful and morally controversial. The figure of Shylock from Shakespeare represents the suspicion faced by Jewish lenders, who were often allowed to charge interest because Christians were forbidden to do so.

Banking grew more powerful when families such as the Medici turned lending into a large, organized business. Their success came from exchange, partnerships, risk management, and political influence.

Later, institutions such as the Amsterdam Exchange Bank, the Swedish Riksbank, and the Bank of England expanded banking into a central feature of national power.

The next major step is the bond market. Governments needed money for war, and bonds allowed them to borrow from citizens and investors.

Italian city-states first used forced loans that later became tradable securities. Over time, bonds became central to public finance, especially in Europe.

Ferguson shows their power through the rise of the Rothschild family. During the Napoleonic Wars, Nathan Rothschild helped Britain obtain gold to finance war efforts.

When Napoleon was defeated sooner than expected, Rothschild shifted strategy and bought British bonds, correctly predicting that their value would rise. This episode shows how information, timing, and confidence could turn finance into political and historical power.

Bonds also reveal the danger of debt and inflation. The American Civil War demonstrates how financial weakness can destroy a political cause.

The Confederacy tried to use cotton-backed bonds to raise money in Europe, but once access to cotton became uncertain, the bonds lost credibility. Without major financial support, the South’s position weakened.

Later, Germany after the First World War and Argentina in the late twentieth century show how inflation and default can devastate bondholders, savers, and entire middle classes. Bonds promise stability, but that promise depends on political order, taxation, credibility, and control of money.

Ferguson then turns to stocks and corporations. The joint-stock company made it possible for investors to pool money, share ownership, and limit personal liability.

This helped fund risky ventures such as overseas trade. Yet the stock market also created bubbles.

A bubble begins when some real change creates new profit opportunities, then optimism drives prices higher, then speculation grows, and finally panic follows when confidence breaks. John Law’s financial experiment in France is the main early example.

Law created a bank, issued paper money, and promoted a trading company linked to France’s American territory. His system expanded credit and excited investors, but it rested on exaggerated promises and personal control.

When confidence collapsed, the bank failed, the shares crashed, and France’s trust in paper money and stock markets was damaged for generations.

The same pattern appears in later markets. The 1929 crash in the United States came after a period of optimism, technological change, rising productivity, and easy credit.

People bought stocks with borrowed money, believing prices would continue to rise. When the crash came, the Federal Reserve failed to prevent the banking system from shrinking credit.

Bank failures and falling money supply turned a financial collapse into the Great Depression. By contrast, after the 1987 crash, the Federal Reserve acted quickly to support liquidity, helping prevent a depression.

Ferguson also compares John Law’s system with Enron. Enron promised to transform energy markets but relied on manipulation, political access, and false accounting.

Its collapse shows that financial invention without honesty can become fraud.

The book then examines risk and insurance. Life is uncertain, and insurance developed as a way to manage loss before it happens.

Hurricane Katrina shows both the importance and limits of private insurance. Many people believed they were protected, only to find gaps in coverage or resistance from insurers.

Ferguson traces modern insurance to Scottish ministers who created a fund for widows by using probability, life expectancy, premiums, and investment returns. This marked a shift from simply saving for disaster to calculating and sharing risk across a group.

From private insurance, Ferguson moves to welfare states. Governments began to provide protection through pensions, health insurance, unemployment support, and public welfare.

Germany under Bismarck helped pioneer this model, while Britain and Japan expanded it greatly. Japan’s welfare system worked well for a time because it was supported by economic growth, social conformity, family structures, and employer loyalty.

In the West, welfare states struggled under individualism, unemployment, inflation, aging populations, and rising costs. Chile became a testing ground for a different approach, influenced by Milton Friedman and market-oriented reformers.

José Piñera helped replace state pensions with private retirement accounts, arguing that ownership and personal responsibility would create better outcomes. Ferguson presents this as part of a larger debate over whether risk should be carried by individuals, markets, or governments.

Housing becomes the next financial frontier. Property has long been tied to power, security, and status.

In Britain, land ownership once supported aristocratic dominance, but declining agricultural income weakened old landowners who had borrowed against their estates. In the United States, mass home ownership grew during the New Deal.

Roosevelt’s reforms changed mortgages by extending repayment periods, supporting amortized loans, and using government backing to encourage lenders. This helped create a home-owning democracy, but racial discrimination excluded many African-Americans through red-lining and unequal credit access.

The dream of safe property later became dangerous. Savings and Loan institutions in the United States took excessive risks after deregulation, knowing deposits were insured by the government.

This created moral hazard and led to huge taxpayer losses. Wall Street then transformed mortgages into tradable securities, which spread housing debt through global markets.

Subprime mortgages expanded home ownership among risky borrowers, but many loans had unstable terms. The system depended on low interest rates, steady employment, and rising house prices.

When those conditions ended, defaults spread through securitized debt and helped trigger the global crisis of 2007.

Finally, Ferguson studies globalization. The nineteenth century saw a major expansion of global finance, trade, and investment under British power.

The Opium War shows the darker side of this system, as Britain used force to open China to trade that served British interests. Global investment grew rapidly before the First World War, and many believed economic interdependence would prevent large-scale conflict.

They were wrong. War shattered confidence, closed markets, disrupted the gold standard, and helped bring a period of de-globalization.

After the Second World War, global finance was rebuilt under institutions such as the IMF and World Bank, but with controls on capital flows. Later, global investment expanded again.

Hedge funds and investors such as George Soros represented a new age of mobile capital. Long-Term Capital Management showed the danger of trusting mathematical models too much.

Its founders understood equations, but underestimated history, panic, and global connection.

The book ends with China and America. China became the manufacturing power, while America became the consumer and borrower.

Chinese savings helped finance American deficits, while American demand supported Chinese exports. Ferguson calls this relationship Chimerica.

It created growth and cheap goods, but also imbalance and dependence. In the end, Ferguson argues that finance evolves like a living system.

It creates progress, but also failure. Markets mirror human behavior, and their crises reveal not only technical mistakes, but also the desires and weaknesses of the people who build them.

Key Figures

Niall Ferguson

Niall Ferguson functions as the guiding intelligence of The Ascent of Money, shaping a vast financial history into a clear argument about civilization. He is not a neutral recorder of facts in the book; he is an interpreter who wants readers to see finance as a central part of human progress rather than as a narrow field reserved for bankers and economists.

His voice is confident, historical, and often cautionary. He repeatedly connects financial instruments to war, empire, poverty, social mobility, and crisis, which gives his role the quality of a narrator who is correcting a common misunderstanding.

Ferguson is especially interested in showing that finance is neither purely evil nor purely liberating. It is a human creation that carries human strengths and flaws.

His character as an author is defined by this balance: he admires innovation, but he does not excuse recklessness.

Money

Money acts almost like the central force of the book. It changes form across history, appearing as silver, coins, clay records, paper notes, bank deposits, bonds, securities, and digital claims.

Its most important quality is not physical substance but trust. Ferguson presents money as powerful because people agree to believe in it.

When that belief holds, societies trade, borrow, invest, build institutions, and expand. When belief breaks, inflation, panic, default, and collapse follow.

Money is also morally complicated. It can fund war, conquest, exploitation, and fraud, yet it can also support enterprise, savings, pensions, home ownership, and recovery.

In this sense, money is not shown as a villain or hero. It is a tool that magnifies the intentions and weaknesses of the people who use it.

Francisco Pizarro and the Spanish Conquistadors

Francisco Pizarro and the Spanish conquistadors represent the violent illusion that precious metal alone equals wealth. Their conquest of the Inca Empire is driven by hunger for gold and silver, and their actions expose the brutality behind early modern imperial extraction.

Pizarro’s role in the book is not only historical but symbolic. He stands for a narrow understanding of money: the belief that wealth is something to seize, melt, ship, and store.

Yet the Spanish experience proves the limits of that belief. The flood of silver from the Americas does not make Spain permanently rich; instead, it contributes to inflation and reveals that value depends on supply, demand, and confidence.

Pizarro’s importance lies in the contrast between conquest and financial understanding. He can take treasure, but he cannot master the system that gives treasure meaning.

The Inca Empire

The Inca Empire is presented as advanced, organized, and wealthy in material terms, yet outside the European money economy. Its people possess gold and silver, but they do not treat these metals as money in the way the Spanish do.

This makes the Incas a crucial contrast in the book’s argument. They show that a society can be complex without using money as Europeans understood it.

At the same time, their fate under Spanish conquest demonstrates how financial concepts became linked to imperial power. The Incas are not simply victims of military defeat; they are drawn into a global system that values their metals differently from the way they do.

Their role helps Ferguson separate wealth as ornament or ritual object from money as a social and economic agreement.

Leonardo Fibonacci

Leonardo Fibonacci appears as a quiet but transformative figure. His importance comes from mathematics, not conquest or political command.

By introducing Hindu-Arabic numerals to Western Europe, he gives merchants and lenders a better language for calculation. In the book, this makes him one of the hidden builders of modern finance.

His work allows interest, fractions, decimals, and commercial accounting to become easier to manage. Fibonacci shows that financial history depends not only on banks and markets, but also on intellectual tools.

Without better numbers, credit remains clumsy and limited. His character represents the power of abstraction: a change in notation can alter trade, debt, lending, and economic growth across centuries.

Shylock and the Jewish Moneylenders

Shylock, though a literary figure, is used to represent real social tensions around money-lending in Europe. In the book, he stands at the meeting point of finance, religion, prejudice, and law.

Jewish moneylenders were often pushed into roles that Christian society needed but publicly condemned. This created a bitter contradiction: borrowers depended on lenders, yet lenders were morally and socially attacked.

Shylock’s role reveals how finance can produce resentment when debt becomes personal and unequal. He also shows how religious rules shaped economic life.

Christian restrictions on usury opened a space for Jewish lenders, but that space came with danger, isolation, and hostility. Through him, the book presents finance as a field where social exclusion and economic necessity often exist together.

The Medici Family

The Medici family represents the movement from small-scale money-lending to organized banking power. In The Ascent of Money, they show how finance can become political authority.

Giovanni di Bicci de’ Medici begins the family’s rise by building a banking operation around currency exchange, bills of exchange, partnerships, and careful risk management. Cosimo de’ Medici then turns financial strength into civic dominance.

The Medici are important because they prove that bankers can become rulers without holding formal crowns. Their power comes from networks, information, credit, and the ability to survive defaults that might destroy smaller lenders.

They also mark a shift in the moral image of finance. Earlier lenders could seem marginal or suspect, but the Medici turn banking into a refined instrument of status, culture, and government influence.

The Bank of England and Central Banking

The Bank of England and other central banks appear as institutional characters rather than individuals. They embody the effort to make money more reliable, flexible, and nationally useful.

Their role grows from financing government war debts into regulating currency, supporting banks, and influencing the wider economy. The Bank of England shows how public authority and private finance became closely linked.

It begins as a solution to state borrowing needs, but over time it becomes a stabilizing force in the financial system. Central banking in the book is presented as both powerful and limited.

It can provide liquidity, issue trusted notes, and shape credit, but it cannot abolish panic, bad judgment, or political pressure. Its character is therefore protective but imperfect.

Nathan Rothschild

Nathan Rothschild is one of the book’s strongest examples of financial intelligence as historical power. His role during and after the Napoleonic Wars shows that information, speed, and judgment can be as decisive as armies.

He is asked to help Britain secure gold for military needs, but his real brilliance appears after Napoleon’s defeat. Instead of being trapped by the sudden loss of demand for gold, he shifts toward British bonds, expecting their value to rise in peacetime.

This decision brings huge profits and cements the Rothschild reputation. Nathan is portrayed as bold, disciplined, and strategically alert.

He also represents the rise of international finance, where private bankers can influence states because governments need credit to fight, survive, and recover.

Napoleon Bonaparte

Napoleon Bonaparte is not a financial thinker in the book, but his wars create the conditions that reveal the power of finance. He represents the military and political force that pushes states into debt and makes bond markets central to survival.

His defeat at Waterloo is important not only because it ends a military era, but because it changes the value of British government bonds and creates an opportunity for Rothschild. Napoleon’s character shows how war and finance are connected.

Armies require money, supplies, credit, and trust. Even a commander of extraordinary ambition cannot escape financial limits.

In the book, Napoleon’s rise and fall help prove that history is not shaped by battlefield decisions alone. Behind military events stands the question of who can pay.

The Confederacy

The Confederacy appears as a political project weakened by financial fragility. Its leaders try to fund war through bonds and by using cotton as collateral, believing that Europe’s dependence on cotton will force support.

For a time, cotton-backed bonds seem clever because they link debt to a valuable commodity. Yet the plan fails when military events disrupt access to cotton and when major financiers such as the Rothschilds refuse to support the Confederate cause.

The Confederacy’s character in the book is proud, risky, and overconfident. It mistakes a valuable crop for a secure financial foundation.

Its collapse shows that credit depends not only on assets, but also on trust, logistics, military control, and political credibility.

John Law

John Law is one of the most fascinating figures in the book because he combines genius, ambition, charm, and recklessness. He understands that money can be based on confidence rather than metal, and he sees that paper money and credit can stimulate an economy.

His bank and Mississippi Company initially seem to offer France a new financial future. Yet Law’s system becomes dangerous because it rests on exaggerated expectations, excessive share issuance, and his own concentration of power.

He promotes colonial wealth that cannot match the dreams sold to investors. When confidence breaks, his entire structure collapses.

Law is not presented as a simple fraud. He is more complex: a man with real insight who loses control because imagination, self-interest, and financial expansion outrun reality.

Kenneth Lay and Enron

Kenneth Lay and Enron serve as a modern echo of John Law’s failure. Lay presents Enron as a company that can transform energy markets, replacing old utilities with a new trading system.

Like Law, he uses political access, bold promises, and financial complexity to create confidence. Yet behind the image of innovation lies manipulation and dishonest accounting.

Enron’s role in the book is to show that modern markets can repeat old mistakes under new language. The company turns opacity into power until the numbers can no longer support the story.

Lay’s character is defined by ambition without sufficient restraint. He represents the danger of treating market confidence as something that can be manufactured indefinitely.

Robert Wallace and Alexander Webster

Robert Wallace and Alexander Webster represent the moral and mathematical origins of modern insurance. Their concern begins with a practical human problem: the families of dead clergymen being left without support.

Instead of relying on charity alone, they create a system based on premiums, investment, probability, and expected mortality. Their role in the book is constructive and humane.

They show finance working not as speculation or conquest, but as protection against uncertainty. Their achievement depends on trust and calculation.

By turning risk into something that can be shared across a group, they help create one of the most important social uses of financial thinking. They are important because they make finance feel less like greed and more like organized care.

Otto von Bismarck

Otto von Bismarck appears as a key figure in the rise of state-backed welfare. His role is practical and political.

By supporting pensions and social insurance, he helps create a model in which the state protects citizens from some of life’s risks. Bismarck’s importance lies in shifting insurance from private arrangements toward national systems.

He recognizes that social stability can be strengthened when workers feel protected against old age, sickness, and insecurity. In the book, this does not make him sentimental; rather, he is shown as a statesman who understands welfare as a tool of order and national strength.

His legacy raises one of the book’s lasting questions: how much risk should individuals carry, and how much should the state absorb?

Milton Friedman

Milton Friedman represents the argument that too much state protection can weaken economies and personal responsibility. His ideas stand against large welfare systems and focus on inflation control, markets, and individual choice.

In the book, his influence is most visible in Chile, where market reforms are used to fight extreme inflation and reduce the role of the state. Friedman’s character is intellectual and ideological.

He is not shown as a conventional political ruler, but as an economist whose ideas shape policy through others. His role is controversial because his reforms are associated with Chile under dictatorship, creating tension between economic success and political morality.

Ferguson uses him to explore the appeal and risk of returning responsibility from the welfare state to the individual.

Augusto Pinochet and José Piñera

Augusto Pinochet and José Piñera together represent the harsh political setting and technical policy design behind Chile’s pension reforms. Pinochet provides the authoritarian environment in which major economic changes can be imposed, while Piñera gives those changes their specific form through Personal Retirement Accounts.

Piñera’s role is especially important because he believes ownership will make workers more responsible and invested in their own futures. The Chilean reforms are presented as economically influential, but they sit inside a troubling political context.

These figures show that financial systems cannot be separated from power. A reform may produce growth or reduce inflation, but the conditions under which it is introduced still matter.

Their role forces the reader to consider both outcomes and legitimacy.

Franklin D. Roosevelt

Franklin D. Roosevelt appears as the architect of mass home ownership in the United States. His New Deal reforms respond to the Great Depression by changing the mortgage system and using government power to restore confidence.

Roosevelt’s role in the book is that of a political leader who understands finance as a democratic tool. By supporting long-term, amortized mortgages and government-backed lending, his administration helps millions of Americans become homeowners.

Yet this achievement is incomplete because African-Americans are often excluded through discriminatory lending practices. Roosevelt’s character in the book is therefore both transformative and limited.

He helps turn property ownership into a pillar of American democracy, but the benefits of that system are distributed unequally.

Margaret Thatcher

Margaret Thatcher represents the later British push toward home ownership and private responsibility. Her policies encourage people to buy public housing and make mortgage ownership more attractive.

In the book, she stands for a political belief that property ownership can create independence, discipline, and social aspiration. Thatcher’s role parallels Roosevelt’s in one sense because both expand home ownership, but her ideological setting is different.

She is linked less to state rescue and more to market-oriented reform. Her character is forceful and practical.

She treats ownership as a way to reshape society, not merely as a housing policy. Through her, the book shows how finance enters everyday identity: to own a home is to become a particular kind of citizen.

Hernando de Soto

Hernando de Soto appears as a thinker who sees hidden wealth among the poor. His argument is that people living in informal settlements often possess property in practice but lack legal title, which prevents them from using that property as collateral.

In the book, he represents a hopeful theory: legal ownership can unlock capital and help the poor enter formal economic life. Yet Ferguson also tests the limits of this idea.

The example of squatters gaining title but rarely obtaining mortgages complicates de Soto’s claims. His role is valuable because he shifts attention from charity to property rights, but his theory is not treated as a complete solution.

He shows that legal title matters, but credit also depends on institutions, income, trust, and lender behavior.

Muhammad Yunus and Women Borrowers

Muhammad Yunus represents a different route to financial inclusion. Instead of requiring property as collateral, he builds microfinance around small loans, trust, group discipline, and especially women borrowers.

His work in Bangladesh challenges the assumption that the poor are poor because they are not creditworthy. In the book, Yunus is important because he shows that small amounts of credit can support enterprise where formal banking fails.

The women borrowers, such as Betty Flores in Bolivia, become evidence that responsibility and repayment are not limited to wealthy borrowers with assets. Their role is practical and corrective.

They show that finance can work from the bottom up when designed around real social behavior rather than only around property ownership.

George Soros

George Soros appears as the emblem of modern hedge fund power. He represents mobile capital, speculation, instinct, and global financial pressure.

His theory of reflexivity gives him a distinct intellectual profile: he believes markets are shaped by investor perceptions, and those perceptions are then changed by market movements. This makes him different from investors who treat markets as purely rational machines.

His famous bet against the British pound shows how a private financier can challenge a national currency. In the book, Soros is not merely a gambler.

He is a reader of market psychology. His success shows the power of judgment in a world where capital can move quickly across borders and expose weak policy decisions.

Long-Term Capital Management

Long-Term Capital Management functions as a collective character built from brilliance and blindness. Its founders, including Myron Scholes, Robert Merton, and John Meriwether, represent the confidence of mathematical finance.

Their models produce huge early returns and carry the authority of Nobel-winning theory. Yet their failure shows that equations can underestimate fear, contagion, and rare events.

LTCM’s character is proud, intelligent, and fragile. It believes it has measured risk better than others, but it has not looked far enough into history or fully understood global connection.

In The Ascent of Money, its collapse becomes a warning against confusing precision with wisdom. The firm knows much about mathematics, but not enough about human panic and historical memory.

China and America

China and America appear together as the final large-scale characters in the book’s financial drama. China becomes the manufacturing and saving power, while America becomes the consuming and borrowing power.

Their relationship is mutually useful but unstable. China sells goods to American consumers, keeps its currency competitive, accumulates dollars, and buys American government debt.

America receives cheap products and low interest rates, but becomes dependent on foreign savings. This pairing shows globalization at its most powerful and most dangerous.

The two nations are not simply rivals or partners; they are locked into a shared financial arrangement. Their character as a pair is defined by imbalance, convenience, and risk.

Themes

Trust as the Foundation of Finance

Finance depends on trust more than metal, buildings, contracts, or equations. The book repeatedly shows that money works only when people believe it will be accepted by others.

Silver from the Americas does not save Spain because the value of money changes when supply overwhelms demand. Paper notes, bank deposits, bonds, insurance policies, mortgages, and securities all require confidence in institutions and future repayment.

When trust exists, credit expands and societies can build banks, fund wars, insure families, buy homes, and connect markets across continents. When trust collapses, the same instruments become dangerous.

Bank runs, bond crashes, failed currencies, and broken stock markets are not only technical events; they are moments when belief disappears. This theme gives the book its deepest unity.

The history of finance is not a march from primitive coins to advanced markets. It is a recurring test of whether people trust the promises behind money.

Every financial instrument is a promise, and every crisis asks whether that promise can still be believed.

Innovation and Instability

Financial innovation creates progress, but it also creates new forms of danger. Banks make lending more efficient, bonds help governments raise money, stock markets allow companies to grow, insurance spreads risk, mortgages expand home ownership, and global capital supports development.

Yet each innovation brings fresh weaknesses. Banks can fail if too many depositors panic.

Bonds can be destroyed by inflation or default. Stocks can inflate into bubbles when excitement outruns earnings.

Insurance can leave gaps when disasters exceed private coverage. Mortgages can become unstable when lenders ignore credit quality and sell risk into global markets.

The book’s pattern is clear: every solution eventually produces new problems. The Ascent of Money presents finance as a living system that adapts, mutates, and sometimes breaks.

Innovation is not condemned, because without it modern civilization would be poorer and less flexible. But innovation without memory, regulation, and humility becomes dangerous.

The same creativity that funds growth can also create instruments so complex that even their creators fail to understand the risks.

Risk, Security, and Responsibility

The question of who should carry risk runs through the book. Individuals face illness, death, unemployment, old age, storms, debt, and market loss.

Private insurance offers one answer by pooling risk among policyholders. Welfare states offer another by making government responsible for pensions, health care, and social protection.

Market reforms offer a third by returning responsibility to individuals through private accounts, property ownership, and investment choice. None of these answers is perfect.

Private insurers may resist paying claims or fail to cover certain disasters. Welfare states can become expensive and strained by aging populations.

Individual responsibility can encourage ownership and discipline, but it can also expose people to losses they do not fully understand. Housing shows this tension clearly.

A home can provide security, status, and collateral, but mortgage debt can also destroy families when prices fall or interest rates rise. The book treats risk as unavoidable.

The real issue is how societies distribute it, price it, and explain it to ordinary people.

Memory, History, and Repeated Mistakes

Financial crises repeat because people forget. Investors believe new markets have escaped old limits, governments assume confidence will last, and experts trust models that ignore rare disasters.

John Law’s bubble, the 1929 crash, Enron, subprime mortgages, and Long-Term Capital Management all show different versions of the same failure: optimism becomes certainty, complexity hides weakness, and warning signs are dismissed. History matters because finance is shaped by human behavior, not only by mathematics.

Fear, greed, ambition, pride, and herd thinking do not disappear when markets become more advanced. They simply operate through newer instruments.

The book’s repeated warning is that technical knowledge without historical memory is incomplete. LTCM’s founders understood formulas but underestimated the lessons of past crashes.

Pre-war investors believed globalization would prevent conflict because they had not lived through a recent European war. The danger is not only ignorance, but overconfidence.

Financial history teaches that systems usually look safest shortly before they reveal their weaknesses.